By Anthony Diosdi

Recently, the Internal Revenue Service (“IRS”) and the Department of Treasury (“Treasury”) issued a number of regulations and proposed regulations (the Proposed Regulations) that will restrict foreign persons’ ability to minimize U.S. tax through “conduit” financing arrangements. See REG-106013-19; 85 F.R. 19858-19873. The new final regulations and Proposed Regulations potentially impact a number of types of structures used by foreign persons for financing into the United States, and therefore these structures should be reevaluated. The discussion below first presents a brief overview of the 30 percent withholding tax as well as the “anti-conduit” rules, then describes if a properly structured “leveraged lease” is entitled to an exemption U.S. withholding tax.

The 30 Percent Withholding Tax

Non-U.S. taxpayers are subject to U.S. federal income taxation on a limited basis. Unlike U.S. taxpayers, who are subject to U.S. federal income tax on their worldwide income, non-U.S. taxpayers are only subject to U.S. taxation on two categories of income. First, non-U.S. taxpayers are subject to U.S. federal income tax on income that is effectively connected to a U.S. trade or business (“ECI”). ECI is taxed on a net basis at the same graduated rates that apply to U.S. taxpayers. Second, non-U.S. taxpayers are subject to U.S. tax on certain passive types of U.S. source income such as interest, dividends, rents, annuities, and certain types of fixed or determinable annual or periodical income. This enumeration is sometimes referred to as “FDAP income.”

Internal Revenue Code Sections 871(a) (for nonresident aliens) and Section 881(a) (for foreign corporations) impose the 30-percent tax on FDAP. Tax treaties generally provide for the reduction or elimination of withholding taxes on specific items of U.S.-source FDAP income that is not attributable to a permanent establishment in the United States. To qualify for treaty benefits, a non-U.S. taxpayer must be a resident of a particular treaty jurisdiction, as well as satisfy the treaty’s limitation of benefits (“LOB”) provision. Even if a non-U.S. taxpayer qualifies for treaty benefits, Sections 7701(1) and 894(c) may prevent a non-U.S. taxpayer from claiming treaty benefits.

Anti- Conduit Rules

In 1993, Congress added Section 7701(1) to the Internal Revenue Code. This provision authorizes the promulgation of regulations allowing for the “recharacterization” of multiple-party financing transactions as a transaction directly among any two or more of the parties to it if such characterization “is appropriate to prevent avoidance of any tax.” The IRS has implemented this authority by issuing so-called “anti-conduit” regulations. The principal result when the new regulations apply when the new regulations apply is that intermediate entities (“conduits”) are disregarded in determining U.S. taxes on international financing arrangements, which may include loans, leases, and licenses. The U.S. tax result will then be determined as if the loan were made directly from the foreign lender to the U.S. borrower. The definational provisions governing the application of the anti-conduit rules are found principally in Treasury Regulation Section 1.881-3 and 4.

The key factors that will trigger the exercise of power by the IRS to recharacterize conduit entities are:

The participation of the intermediate entity or entities reduces the tax imposed by Section 881.

Such participation is “pursuant to a tax avoidance plan,” and either

The intermediate entity is related to the finance or financed entity or would not have participated in the financing arrangement but for the fact that the financing entity engaged in the transaction with the intermediate entity. See Treas. Reg. Section 1.881-3(a)(4).

The regulations also identify the factors that will determine whether there is a tax-avoidance purpose:

Is there a “significant reduction” in the tax otherwise imposed under Section 881?

Did the conduit have the ability to make the advance without advances from the related financing entity?

What was the period of time between the respective transactions?

Did the financing transactions occur in the ordinary course of business of the related entities?

The regulations also establish a rebuttable presumption in favor of the taxpayer if the conduit entity “performs significant financing activities with respect to the financing transactions forming part of the financing arrangement.” Such activities might include the earning of rents and royalties from the active conduct of a trade or business or active risk management by the intermediate entity. See Treas. Reg. Section 1.881-3(b)(3).

The effect of invoking the anti-conduit regulations is that the payments will be deemed to be paid directly by and to the entities other than the conduit, usually the financing or financed. The role of the conduit will be disregarded. If these provisions were invoked in the case of a finance subsidiary, for example, the interest payment by a U.S. corporation that borrowed money from a foreign lender through the use of a financing subsidiary in a tax treaty country would be treated as if the interest were paid directly to the foreign lender. The treaty would not apply, and the 30-percent withholding tax would be imposed unless the “true” lender were a resident of another treaty country where withholding rates on interest were reduced or eliminated. The borrower is required to withhold the appropriate amount under the recharacterized transaction. See Treas. Reg. Sections 1.1441-3(g) and 7(f).

For an intermediate entity (or related entities taken together) to be a conduit entity, all three tests below must be satisfied:

1. The participation of the intermediate entity reduces the tax imposed under Section 881 of the Internal Revenue Code (i.e. the withholding tax);

2. The intermediate entity participates in the financing arrangement pursuant to a “tax avoidance plan;” and;

3. The intermediate entity is related to the financing entity or the financed entity, or the intermediate entity would not have participated in the financing arrangement on substantially similar terms but for the fact that the financing engaged in the financing transaction with the intermediate entity.

When (1) and (2) apply, the IRS has authority to disregard the participation of the intermediate entity(ies) so that the payment flow is treated as going directly from the financed entity to the financing entity with the appropriate withholding tax consequences.

Tax Treaties and Hybrid Entities

Internal Revenue Code Section 894(c) denies tax treaty benefits when a non-U.S. taxpayer invests in the United States through an entity that is “fiscally transparent” or is an entity that is a “hybrid” under the laws of the United States or any other foreign country. Issues involving “hybrid entities” arise in a number of different contexts in the taxation of international transitions. A hybrid entity is one that is characterized as a corporation in one jurisdiction and a transparent entity in another. For example, an entity organized in a foreign country may be treated as a corporation under the laws of that country, but may be treated as a partnership under U.S. tax law. The reverse situation (often called a “reverse hybrid”) may also be obtained when an entity is treated as a corporation under U.S. tax law, but as a transparent entity under the laws of a foreign country. Such situations may lead to opportunities for cross-border arbitrage in which the tax laws of the different countries are exploited for multiple advantage.

Internal Revenue Code Section 894(c) expressly limits the availability of treaty benefits in certain hybrid situations and authorizes the promulgation of regulations to defend against perceived treaty abuse in other hybrid situations.

Internal Revenue Code Section 894(c)(1) also denies benefits for income derived through a partnership or other entity treated as transparent for U.S. tax purposes in certain situations even though the partner is a resident of a foreign treaty country. The application of the provision depends largely upon the law of the treaty country. Withholding tax reductions or exemptions provided in a treaty will be denied to a partner, even if the entity is treated as a partnership or other transparent entity under U.S. tax law, if the item of income is not treated under the tax law of the treaty country as income of the partner, the treaty itself contains no provisions addressing its applicability in the case of income derived through a partnership and the foreign treaty country does not tax the distribution of such item of income from the partnership to the partner.

Extensive regulations have been promulgated under the authority of Section 984(c)(2). The regulations clarify the application of treaty benefits in a number of situations. If the entity is classified as a partnership under U.S. tax law, the availability of treaty benefits will normally depend upon whether the entity is classified as a transparent entity under the laws of its place of organization and, if so, whether the laws of the place of residency of an interest holder in the foreign entity treat that entity as a transparent entity. If the entity is not classified as a transparent entity in the foreign country in which it is organized, the taxpayer will be treated as the entity itself and any treaty benefits applicable to a resident of the country of organization will be available. Treaty benefits will also be available when there is a treaty between the United States and the interest holder’s country and if the laws of that country characterize the entity as a fiscally transparent entity. In any case, an item of income paid directly to a type of entity specifically identified in a treaty as a resident of a treaty country is treated as derived by a resident of the treaty jurisdiction entitled to treaty benefits. See Treas. Reg. Section 1.894-1(d)(1).

The regulations further provide that treaty benefits will not be available to foreign interest holders of an entity classified as a corporation under U.S. law, even though the entity may be classified as a transparent entity under the laws of a treaty country paid by an domestic entity classified as a corporation under U.S. law will be treated as income to interest holders regardless of the classification of the entity under foreign law and the character of the income will be determined by applying U.S. legal standards. As such, the foreign interest holder may be subject to tax, but will be entitled to any treaty benefits that might apply. If the foreign interest holder is a transparent entity under the laws of its place of organization, the tax consequences of such payments, including the possible availability of treaty benefits will depend upon the identity of partners or members of the foreign entity. See Treas. Reg. Section 1.894-1(d)(2)(ii)(A).

For example, suppose that a foreign entity is treated as a partnership for U.S. tax purposes. It is organized in Country A, with which the United States has no income tax treaty. One of the partners, Partner X is a citizen and resident of Country B, with which the United States has a tax treaty that is identical to the U.S. Model Treaty. However, the entity is treated as a corporation under the laws of Country A and Country B. The foreign entity, organized in Country A, realizes U.S. source interest income, a portion of which is allocable under U.S. federal tax law to Partner B. U.S. source interest payments to corporations organized in Country A are subject to a withholding tax of 30 percent. U.S. sourced interest payments to Partner X, as a resident of Country B, would be exempt from tax under the treaty with Country B. Since Partner X is not subject to tax in Country B (the treaty country) on income realized by the entity (because it is treated as a corporation under the laws of Country B), Section 894(c)(1) applies and Partner X is not entitled to the treaty exemption for interest payments from U.S. sources. See Taxation of Internal Transactions,Thompson West, (2005), Charles H. Gustafson, Robert J. Peroni, and Richard Crwford Pugh at 4102.

Treasury Regulation Section 1.8881-3(a)(1) also allows the IRS to disregard the participation of one or more “intermediate entities” in a “financing arrangement” where such entities are acting as conduit entities. For example, suppose A lends money to B, for which B pays interest to A, and B turns around and lends that money to C, for which C pays interest to B.

The regulations give the IRS authority to collapse the loan and treat A as having lent money to C. As a result, the IRS will treat A, rather than B, as having derived interest from C for purposes of the 30 percent withholding tax. In the language of the preamble, the conduit regulations permit the IRS “to disregard, for purposes of Section 881, the participation of one or more intermediate entities in a financing arrangement where such entities are acting as conduit entities.” See Treas. Reg. Section 1.881-3(a)(1). In this example, B is the conduit entity, and the IRS is disregarding B’s participation in the loan because it appears that the parties intended the loan proceeds from A-to-B loan to go to C.

The IRS has this authority only when collapsing the loans would increase the amount of the tax. Thus, the IRS can treat A as lending directly to C only if A would be subject to more tax than would B on interest derived from C. The tax owed by A could be higher than the tax owed by B for many reasons. For example, if A is not entitled to a treaty exemption or the portfolio interest exemption to which B would be entitled. A would owe more tax than B if the loans were collapsed.

For the IRS to exercise its authority to collapse a transaction, the regulations define a financing arrangement as: a series of transactions by which one person (the financing entity) advances money or other property….and another person (the financed entity) receives money or other property,…if the advance and receipt are effected through one or more other persons (intermediate entities) and…there are financing transactions linking the financing entity, each of the intermediate entities, and the financed entity.

The conduit regulations treat a disregarded entity as a person. Please see Illustration 1 which provides an example when a conduit is treated as a person:

Illustration 1.

On January 1, 1996, Foreign Parent (“FP”) lends $1 million to Domestic Subsidiary (“DS”) in exchange for a note issued by DS. On January 1, 1997, FP assigns the DS note to Foreign Subsidiary (“FS”) in exchange for a note issued by FS. After receiving notice of the assignment, DS remits payment due under its note to FS. FS is an entity that is disregarded as an entity separate from its owner, FP. See Treas. Reg. Section 1.881-3(e), Ex. 3.

In the above illustration, FS is treated as an intermediate entity, the DS note held by FS and the FS note held by FP as financing transactions, and the two transactions together as a financing arrangement. Thus, if a foreign person were to lend funds directly to a U.S. borrower, the foreign person’s interest income would be subject to a 30 percent withholding tax. However, if a foreign person could advance funds as an equity investment in an entity that is a resident in a country that has an income tax treaty with the United States and that qualifies for benefits under the treaty, with some limited exceptions, this arrangement was not subject to attack under the anti-conduit regulations.

Please see Illustration 2 which provides such an example:

Illustration 2.

A issues its debt to B in exchange for the stock of B’s subsidiary, C. B controls both A and C for purposes of Section 304 (the basic purpose of Section 304 is to prevent bailouts of corporate earnings at capital gains rates), so the issuance is a distribution by A of its (and, if necessary, C’s) earnings and profits to B. D, another member of the group, advances cash to B in exchange for B’s debt.

D’s advance of cash to B is clearly an advance of money. Is B’s transfer of C stock to A an advance of other property? Apparently so, even though we tend to think of the prototypical conduit situations as an advance of money by a Cayman Islands company to a Dutch company to a U.S. company. See Tax Notes, Volume 146, Number 9, April 27, 2015, The Conduit Regulations Revisited, by Peter M. Daub at 413.

Given that stock acquisition or transfers typically did not constitute a financing transaction, it was common under prior law for non-U.S. taxpayers to utilize a hybrid instrument (e.g., an instrument treated as debt for foreign tax purposes but equity for U.S. tax purposes). On April 7, 2020, the Treasury and IRS released regulations that finalized 2018 Proposed Regulations addressing rules under Sections 267A and 1503(d). On the same date, Treasury and the IRS issued additional 2020 Proposed Regulations under Section 881 (with respect to the “anti-conduit regulations”). These new rules will not only significantly impact cross-border multi-party financing transactions, the new anti-conduit rules have eliminated a number of common tax planning structures with respect to the licensing of intellectual property (“IP”) for use in the United States. Intermediate entities were often used in inbound IP tax planning structures.

The New Final and Proposed Anti-Conduit Regulations

The Anti-Conduit Regulations permit the IRS to disregard, for purposes of Sections 871, 881, and 1442, one or more intermediate entities in a ‘financing arrangement’ if these entities act as ‘conduit entities.’ A financing arrangement involves one person (the financing entity) advancing money or other property, and another person (the financed entity) receiving money or other property through one or more persons (the immediate entities) and there are financing transactions (i.e., debt, a lease or license) linking the financing entity, each of the intermediate entities, and the financed entity.

As a general matter, holding an equity interest does not constitute a financing transaction for purposes of the anti-conduit rules under Treasury Regulation unless such equity qualifies as “Debt-:Line Stock’ under Treasury Regulation Section 1.881-3(a)(2)(ii)(B)(1), that is, as stock in a corporation (or a similar interest in a partnership, trust, other other person) that is subject to certain redemption, acquisition, or payment rights or requirements.

The 2020 Proposed Section 881 Regulations expand the definition of Debt-Like Stock by taking into account the tax treatment of the instrument under the tax law of the equity issuer. Accordingly, the 2020 Proposed Section 881 Regulations create two new categories of equity that constitute a financing transaction: 1) an equity interest with respect to which the issuer is allowed a tax benefit (i.e., a deduction) for an amount paid, accrued, or distributed with respect to such interest either under the laws of the issuer’s country of residence or a country in which the issuer has a taxable presence (i.e. a permanent establishment) to which a payment on a financing transaction is attributable; or 2) an equity interest with respect to which a person related to the issuer is allowed a refund (including a credit) or similar tax benefit for taxes paid by the issuer to its country of residence, without regard to the related person’s tax liability under the laws of the issuer. See Final Section 267A regulations: Additional analysis, Tax Insights from Global Structuring, PWC, April 17, 2020.

The new regulations promulgated by the IRS and Treasury include instruments that are stock (or partnership interest) for U.S. tax purposes, but are treated as debt under the tax law of the country of which the issuer is a tax resident under the anti-conduit rules. See Treas. Reg. Section 1.881-3(a)(2)(ii)(B)(1)(iv). As a result, a non-U.S. taxpayer can no longer utilize U.S. income tax treaty benefits to eliminate withholding on U.S. source royalty payment if it capitalized a foreign licensor with a hybrid instrument for purposes of reducing foreign income tax of the licensor.

In addition, the final regulations provide that if the issuer is not a tax resident of any country, such as an entity treated as a partnership under foreign tax law, the instrument is a financing transaction if the instrument is debt under the tax law of the country where the issuer is created, organized, or otherwise established.

Accordingly, a non-U.S. taxpayer will no longer be able to claim U.S. income tax treaty benefits on the receipt of a U.S. source royalty payment if it capitalizes the foreign licensor with a hybrid instrument in order to reduce the foreign income tax of such licensor. See Treas. Reg. Section 1.881-3(a)(2)(ii)(B)(1)(iv).

Possible Exception to the Anti-Conduit Regulations

As discussed above, the regulations now include in the definition of a financing transaction an instrument that includes stock or a similar interest such as an interest in a partnership. However, the regulations do not address if U.S. source royalty would be ineligible for treaty benefits if the foreign licensor makes interest payments on the related loan. As indicated above, a loan followed by a license will likely be classified as a conduit financing arrangement.

However, where the character of the payment made by the financed entity is different from the character of the payment made to the financing entity, the regulations provide that the character of the payment made by the financed entity is characterized by reference to the character of the payment made to the financing entity. See Treas. Reg. Section 1.881-3(a)(3)(ii)(B). In other words, where a royalty payment is followed by an interest payment, the royalty is recharacterized as interest. See Tax Planning for Inbound Licenses of IP: What is Left After Tax Reform? The Florida Bar, Volume 95, No1 January/February 2021, by Jeffrey L. Rubinger and Summer A. LePree.

The preamble to the 1995 final conduit financing regulations appears to support such an exclusion. In the preamble, the IRS noted that some commentators suggested that leveraged leases be excluded from the definition of a financing transaction because, “in substance, the financing arrangement would be the equivalent of a loan from a financing entity entitled to a zero rate of withholding on interest. The IRS agreed with this comment and noted in the preamble that, under the final regulations, a “leveraged lease generally will not be recharacterized as a conduit arrangement if the ultimate lender would be entitled to an exemption from withholding tax on interest received from the financed entity, even if rental payments made by the financed entity to the financing entity would have been subject to withholding tax.” This language would seem to support the position that a leveraged acquisition of IP by a foreign licensor followed by a license of such IP for the use in the U.S. should be exempted from the conduit financing regulations, if the ultimate non-U.S. lender would be eligible for an exemption from U.S. withholding tax on the receipt of interest from the financed entity. See Tax Planning for Inbound Licenses of IP: What is Left After Tax Reform? The Florida Bar, Volume 95, No1 January/February 2021, by Jeffrey L. Rubinger and Summer A. LePree.

There are some limitations to this rule, however. The regulations indicate that the characterization of the payment as interest will not extend to qualification of a payment for any exemption from withholding tax under the Internal Revenue Code or a provision of any applicable tax treaty if such qualification depends on the terms of, or other similar facts or circumstances related to, the financing transaction to which the financing entity is a party. Therefore, it would seem that so long as the financing entity would be entitled to an exemption from withholding under an income tax treaty, the conduit financing regulations should not apply to a leveraged acquisition of IP. See Tax Planning for Inbound Licenses of IP: What is Left After Tax Reform? The Florida Bar, Volume 95, No1 January/February 2021, by Jeffrey L. Rubinger and Summer A. LePree.

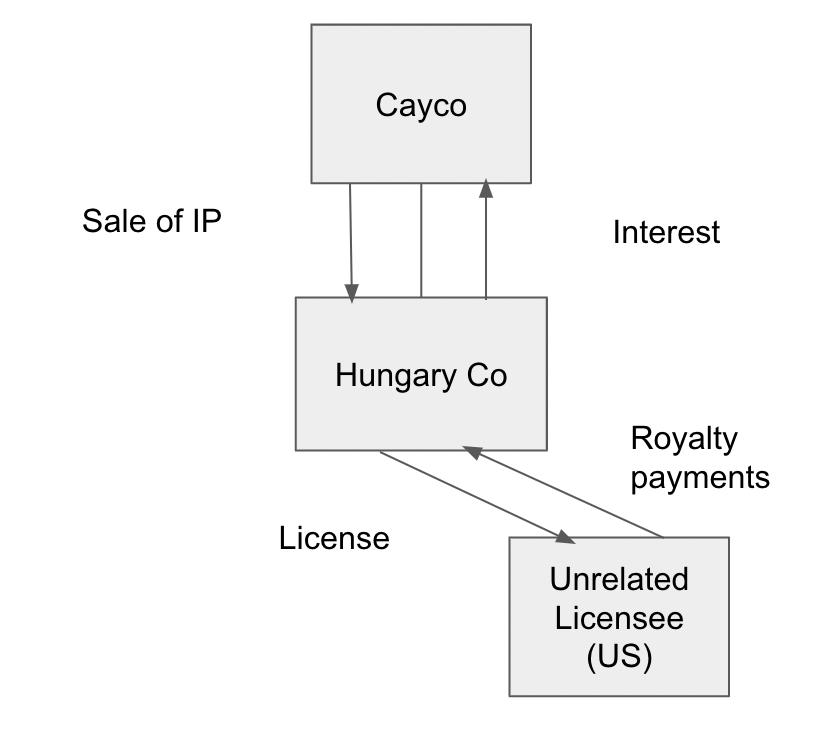

One structure that may be considered in inbound IP license transactions is to license IP to a Hungarian entity. The U.S.-Hungarian tax treaty is one of the few remaining treaties that does not contain a LOB. Since the U.S.-Hungarian tax treaty does not contain a LOB, it allows for a number of interesting planning opportunities. Below, please see an example how a leverage license structure can be set up through the use of the U.S.-Hungarian tax treaty.

Leverage License Example

Cayco owns valuable IP and wishes to license the IP to an unrelated U.S. licensee. Royalties would be subject to 30 percent withholding. Cayco forms Hungarian sub, which is opaque for U.S. and Hungarian purposes, and sells IP to Hungary Co for a note. U.S.-Hungary treaty has no LOB provision and provides source country exemption from withholding tax on royalties. Hungary Co licenses IP to unrelated U.S. licensee in exchange for royalties. Hungary Co is not a hybrid entity, and neither license nor note are hybrid instruments. Though both license and loan are financing transactions under conduit financing regulations, because loan from Cayco to unrelated U.S. licensee would have qualified for exemption from U.S. withholding tax under Internal Revenue Code Section 881(c) and the conduit financing rules do not apply. The preamble to 1995 final conduit financing regulations supports excluding leveraged licenses from their scope. A leveraged lease generally would be entitled to an exemption from withholding tax on interest received from the financed entity, even if rental payments made by the financed entity to the financing entity would have been subject to withholding tax. See Final Anti-Hybrid Rules, Baker McKenzie, Tax News and Developments North America, July 15, 2020, Jeff Rubinger and Summer Ayers LePree.

Anthony Diosdi is one of several tax attorneys and international tax attorneys at Diosdi Ching & Liu, LLP. As a domestic and international tax attorney, Anthony Diosdi provides international tax advice to individuals, closely held entities, and publicly traded corporations. He has also assisted clients in establishing Hungarian structures. Diosdi Ching & Liu, LLP has offices in San Francisco, California, Pleasanton, California and Fort Lauderdale, Florida. Anthony Diosdi advises clients in international tax matters throughout the United States. Anthony Diosdi may be reached at (415) 318-3990 or by email: adiosdi@sftaxcounsel.com.

This article is not legal or tax advice. If you are in need of legal or tax advice, you should immediately consult a licensed attorney.