By Anthony Diosdi

It has been more than 25 years since Congress enacted Section 7701(1) of the Internal Revenue Code and the Department of Treasury (“Treasury”). These provisions authorize the Internal Revenue Service (“IRS”) to recharacterize any multiple-party financing transaction as a transaction directly between two or more parties if it is determined that reclassification is necessary to prevent the avoidance of U.S. tax. Last year, on April 8, 2020, Treasury issued new proposed regulations which would make changes to the current conduit regulations. Anyone involved in the planning of multinational corporate finance transactions, must understand the conduit regulations. This article is designed to provide an introduction to the conduit finance rules which govern the transfer of funds among subsidiaries in different countries.

The 30 Percent Withholding Tax

Historically, foreign taxpayers have utilized financing arrangements to avoid the 30 percent withholding tax. We tend to think of the prototypical foreign taxpayer as an individual investor from a foreign country. However, multinational corporations often get caught up in the withholding rules. By way of background, there is a U.S. federal income tax of 30 percent on a foreign taxpayer’s U.S. source “fixed or determinable, annual or periodical income.” This includes such items of income as interest, dividends, rents, and royalties. The 30 percent withholding tax is imposed on gross income, with no deductions allowed. This tax is assessed on gross income, with no deductions permitted. As a general rule, this tax is collected through withholding, and as a result, it is commonly known as a 30 percent “withholding tax.” Although U.S. source interest, dividends, rents, and royalties are subject to a statutory 30 percent U.S. withholding tax, many bilateral U.S. income tax treaties completely eliminate this withholding tax.

The Anti-Conduit Rules

Congress became aware of numerous “conduit” structures that foreign persons were utilizing to minimize or eliminate the 30 percent withholding tax. One such example would be a foreign person who resides in a country that does not have an income tax treaty with the United States but sets up an entity in a country that does have a treaty with the U.S. Consequently, if that foreign person were to lend funds directly to a U.S. borrower, the foreign person’s interest income would be subject to the 30 percent withholding tax. On the other hand, the foreign person could loan funds to a company that is: 1) a tax resident in a country that has an income tax treaty with the United States that reduces or eliminates the 30 percent withholding tax and 2) that qualifies for benefits under that treaty. This company could then on-lend the funds to the U.S. borrower.

In 1993, Congress enacted Internal Revenue Code Section 7701(1). The Treasury was authorized under Internal Revenue Code Section 7701(1) to issue regulations that would allow multi-party financing arrangements to be reclassified as transactions directly between any two or more parties involved. In accordance with Section 7701(1), the Treasury introduced regulations in 1995 to clarify when the IRS can recharacterize multi-party financing transactions for U.S. withholding tax purposes. Under these regulations, an IRS direct director can ignore the involvement of an intermediate entity in a multi-party financial arrangement for withholding tax purposes if the intermediate entity is deemed to be a conduit entity. A conduit entity is one whose participation in the financing arrangement is designed to minimize U.S. withholding tax liability and is part of a tax avoidance plan, and is one that is either related to the financing/financed entity or entered into the transaction as a result of the financing entity.

Scope of the Anti-Conduit and Proposed Anti-Conduit Regulations

In general, the regulations allow the IRS to disregard the participation of one or more “intermediate entities” in a “financing arrangement” where such entities are acting as conduit entities. The regulations define a financing arrangement as a series of financing transactions by which one person (the financing entity) advances money or other property, or grants rights to use property, and another person (the financed entity) receives money or other property, or rights to use property, if the advance and receipt are effected through one or more other persons (intermediate entities). See Treas. Reg. Section 1.881-3(a)(2)(i)(1)(A). The regulations grant the IRS discretion to disregard, for purposes of Internal Revenue Code Sections 871, 881, 1441, and 1442, the participation of one or more “intermediate entities” in certain “financing arrangements” involving multiple parties.

Under the current regulations, a financing transaction included a debt, lease or license. See Treas. Reg. Section 1.881-3(a)(2)(ii)(A). However, with certain exceptions, these same regulations, an instrument that was classified as equity for U.S. tax purposes cannot constitute a financing transaction. As such, it was common for non-U.S. taxpayers to use a hybrid interest (an instrument treated as debt for foreign tax purposes but equity for U.S. tax purposes) in cross-border financing transactions to avoid the 30 percent withholding tax. In this situation, the payment of a U.S. person or entity to a foreign person or entity, followed by a payment that was treated as interest for foreign tax purposes, was typically not subject to the conduit financing regulations because the U.S. treated the subsequent interest payment as a dividend.

Last year, the IRS and Treasury issued proposed anti-conduit regulations. These regulations will cause the conduit financing regulations to expand the types of equity interests that are treated as financing transactions. The regulations will include a financing transaction so-called hybrid instruments.

An understanding of these terms is necessary to determine when a financing arrangement could be recharacterized under the regulations. We will next discuss the terms that make up a financing arrangement and when the anti-conduit rules could be triggered.

For the IRS to exercise its authority to collapse a transaction, there must be a financing arrangement. The regulations define a financing arrangement as: a series of transactions by which one person (the financing entity) advances money or other property,…and another person (the financed entity) receives money or other property,…if the advance and receipt are effected through one or more other persons (intermediate entities) and…there are financing transactions linking the financing entity, each of the intermediate entities, and the finance entity. However, just because foreign taxpayers utilize a cross-border financing transaction does not automatically mean that the IRS can collapse the transaction. Whether or not the IRS has the legal authority to set aside a financing transaction depends whether or not the transaction was structured correctly. We will now walk through each element of a cross-border financing transaction and discuss areas

Defining The Advance of Money or Other Property

In order to have a financing transaction, there must be debt and an advance of money or other property through one or more persons or entities. Under the regulations promulgated by the Treasury in 1995, instruments treated as debt for foreign tax purposes but equity for U.S. tax purposes did not constitute a financing transaction. Thus, it was common for non-U.S. taxpayers in multinational cross-border transactions to utilize a hybrid instrument (an instrument treated as debt for foreign purposes but equity for U.S. purposes).

For example, A issues its debt to B in exchange for the stock of B’s subsidiary, C. B controls both A and C for purposes of Section 304 of the Internal Revenue Code, so the issuance is a distribution by A of its (and, if necessary, C’s) earnings and profits to B. D, another member of the group, advances cash to B in exchange for B’s debt. D’s advance of cash to B was clearly an advance of money. A hybrid instrument is executed between D and B. Under the 1995 regulations, the utilization of a hybrid instrument was not subject to anti-conduit financing regulations. However, under the Proposed Regulations, if a financing entity, (D in the above example) advances cash or other property to an intermediate entity (B in the example above) through a hybrid instrument, the transaction between D and B will be subject to the anti-conduit transaction rules and collapsed by the IRS.

Defining a Series of Transactions

The next important question raised by the conduit regulations is whether or not “a series of transactions” exists. Multinational corporations often transfer funds between subsidiaries in different countries. If the IRS sees these transitions as isolated from one another, no financing arrangement can be said to exit. If, however, the IRS views these transfers of such funds as a series of transactions, this type of transaction could be collapsed under the anti-conduit regulation. Unfortunately, regulations issued in 1995 and the newly promulgated regulations do not provide any guidance to determine when a series of transactions can be considered as part of a final arrangement that will trigger the anti-conduit rules.

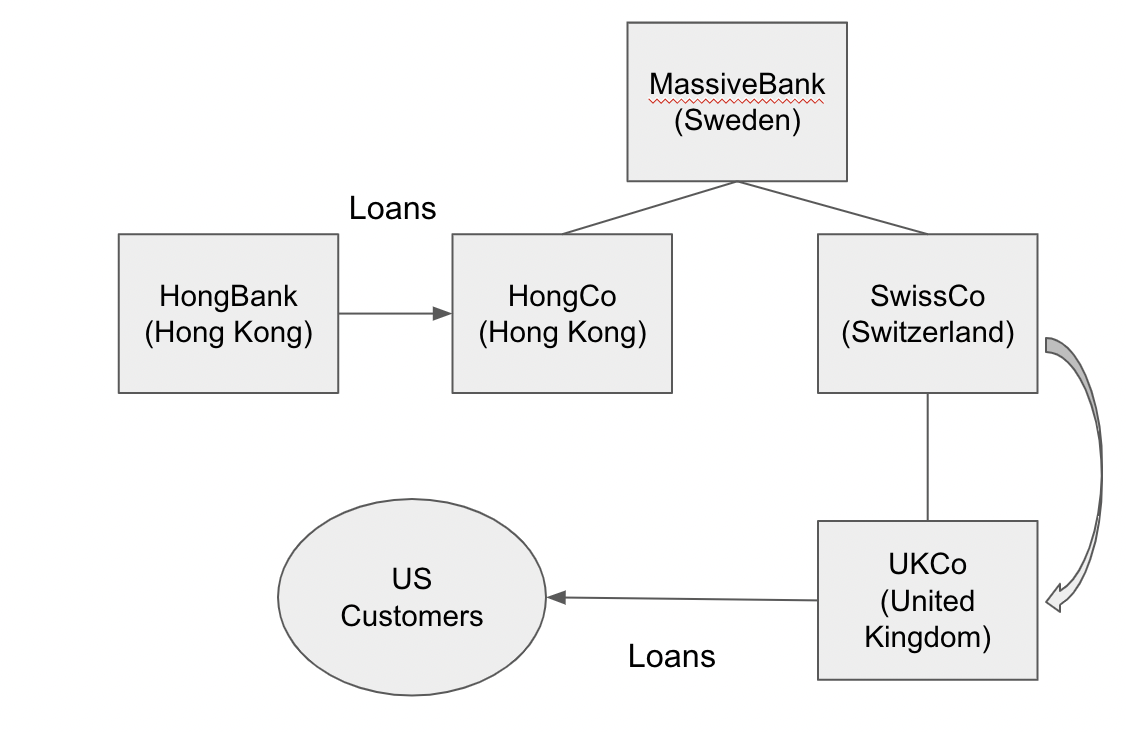

Let’s consider the following example:

MassiveBank, a Swedish-based bank, indirectly owns a bank subsidiary organized in the United Kingdom (UKCo) that occasionally makes loans to customers that reside in the United States. Interest on the loans is exempt from U.S. tax under the U.K-U.S. income tax treaty. A Swiss entity (SwissCo) directly owns UKCo’s finances and makes loans for the purposes of lending to UK customers. Under the U.S. Swiss treaty, Swiss Co would be eligible for exemption from withholding tax on U.S. source interest paid to it. All members of the MassiveBank group that received interest directly from the U.S. customers would not be subject to the 30 percent tax on the interest under a tax treaty exemption.

A Hong Kong non-bank subsidiary of MassiveBank (HongCo), whose operations are separate from those of UKCo, borrows money from a Hong Kong Bank, (HongBank) on a long-term basis to finance the export sales of Hong Kong businesses. Interest derived by HongBank, if deemed derived from U.S. borrowers, would not be eligible for a treaty exemption.

This example demonstrates the difficulty of determining whether a series of transactions exists, and thus whether there is a potential problem under the conduit regulations. The issue is whether, in planning a series of plainly related transactions that should not be recharacterized under the conduit regulations, a group can isolate those transactions from unrelated transactions that it may undertake now or in the future and that the IRS might attempt to link to the series.

A financing arrangement involving UKCo, and U.S. customers would not present a problem because UKCo would be eligible for a treaty exemption and a direct loan from UKCo to U.S. customers therefore would not trigger U.S. withholding tax. Because the participation of SwissCo does not reduce U.S. tax, that financing arrangement would not cause UKco to be considered the lender to the U.S. customers. See Treas. Reg. Section 1.881-3(a)(4)(i)(A).

Even a financing arrangement that also involved HongBank would probably not cause a problem. This is because UKCo’s participation in that financing arrangement would not likely be deemed a tax avoidance plan (a tax avoidance plan is one of the requisites for exercise of the IRS’s authority). As discussed below, two of the factors pointing toward the presence of a tax avoidance plan would be absent because of UKCo’s ability to make an advance from its own funds and the lack of synchronicity between HongBank loans and either the UKCo or SwissCo loans. Thus, the loan from UKCo, even if deemed to have been made directly to the U.S. borrowers, should be respected. On this basis, any loan from HongBank, even if not respected under the regulations as made to HongCo, would, if deemed made to UKCo, be reclassified under the regulations as a transaction directly between the remaining parties to the financing arrangement. Interest, derived by HongCo from UKCo would be foreign-source income and not subject to the 30 percent withholding tax. However, a direct loan from HongBank to the U.S. customers would not likely qualify for an exemption to the 30 percent withholding tax.

The Rules Regarding Disregarding an Intermediate Entity

If the IRS were to disregard the participation of a conduit entity, the financing arrangement will be reclassified as a transaction directly between the financed and the financing entities. For example, assume a foreign parent (FP) located in a jurisdiction that does not have a tax treaty with the United States lends money to a foreign affiliate (FA) located in a jurisdiction that does not have a tax treaty with the U.S. The foreign affiliate then lends money to a U.S. affiliate (Uncle Sam) so that the payments out of the United States are subject to no withholding tax under a tax treaty with FA’s jurisdiction.

The conduit financing regulations permit the IRS to treat this transaction as a loan directly from FP to Uncle Sam so that interest payments are treated, for U.S. tax purposes, as going from Uncle Sam directly to FP.

A Tax Avoidance Plan Needs to be Established Before the IRS May Disregard a Conduit Entity

Once the existence of a financing arrangement has been established, an intermediate entity will be treated as a conduit if the intermediary’s participation in the financing arrangement is under a tax avoidance plan. The regulations describe a tax avoidance plan as:

A plan of which the principal purposes is the avoidance of tax imposed by Section 881 (the 30 percent tax). Avoidance of the tax imposed by Section 881 may be one of the principal purposes for such a plan even though it is outweighed by other purposes (taken together or separately). In this regard, the only relevant purpose are those pertaining to the participation of the intermediate entity in the financing arrangement and not those pertaining to the existence of a financing arrangement as a whole…In determining whether there is a tax avoidance plan, the district director will weigh all relevant evidence regarding the purpose for the intermediate entity’s participation in the financing arrangement. See Treas. Reg. Section 1.881-3(b)(1).

The regulations list three nonexclusive factors to be considered in determining whether the participation of an intermediate entity has as one of its principal purposes the reduction of the 30 percent tax: 1) whether the transaction results in a significant reduction of tax; 2) whether the intermediate entity had the ability to make the advance without advances from the financing entity; and 3) the length of time between the financing transitions. See Treas. Reg. Section 1.881-3(b)(2).

1. Was There a Significant Reduction in Withholding Tax?

The first factor in determining whether or not a tax avoidance plan existed is to determine if the transaction results in a significant reduction of the 30 percent withholding tax. The conduit regulations provide two examples of a significant tax reduction. In one case, the participation of the intermediate entity reduces the tax rate from the 30 percent rate to zero, and, in the other case, it reduces the tax rate from a blended rate from a blended rate (after application of a treaty benefit) of 27 percent to zero. See Treas. Reg. Section 1.881-3(e), Example 14. Because these are large reductions in percentage terms- from 100 percent and 90 percent of the statutory rate, respectively, to zero, the reductions are fairly obviously “significant” and not particularly helpful in determining when a rate reduction is not significant. These are easy examples to follow. It is not too difficult to imagine a far more complicated senior. Just such a scenario detailed in the regulations.

For example, assume FP owns a 10 percent interest in the profits and capital of FX, a partnership organized in country N. The other 90 percent interest in FX is owned by G, an unrelated corporation that is organized in country T. FXis not engaged in business in the United States. On January 1, 1996, FP contributed $10,000,000 to FX in exchange for an instrument documented as perpetual subordinated debt that provides for quarterly interest payments at 9 percent annum. Under the terms of the instrument, payments on the perpetual subordinated debt do not otherwise affect the allocation of income between the partners. FP has the right to require the liquidation of FX if FX fails to make an interest payment. For U.S. tax purposes, the perpetual subordinated debt constitutes guaranteed payments within the meaning of Section 707(c). On July 1, 1996, FX made a loan of $10,000,000 to DS in exchange for a 7-year note paying interest at 8 percent per annum.

Because FP has the effective right to force payment of the “interest” on the perpetual subordinated debt, the instrument constitutes a financing transaction with the meaning of the regulations. Moreover, because the note between FX and DS is a financing transaction within the meaning of the regulations, together the transactions are a financing arrangement within the meaning of the regulations. Without regard to the conduit regulations, 90 percent of each interest payment received by FX would be treated as exempt from U.S. withholding tax because it is beneficially owned by G, while 10 percent would be subject to a 30 percent withholding tax because it is beneficially owned by FP. If FP held directly the note issued by DS, 100 percent of the interest payments on the note would have been subject to the 30 percent withholding tax. The significant reduction in the tax imposed by Section 881 resulting from the participation of FX in the financing arrangement is evidence that the participation of FX in financing arrangement is pursuant to a tax avoidance plan. However, other facts relevant to the presence of such a plan must also be taken into account. See Treas. Reg. Section 1.881-3(e), Example 16.

A more difficult example follows:

Over a period of years, FP has maintained a deposit with BK, a bank organized in the United States, that is unrelated to FP and its subsidiaries. FP often sells goods and purchases raw materials in the United States. FP opened the bank account with BK in order to facilitate this business and the amounts it maintains in the account are reasonably related to its dollar-denominated working capital needs. On January 1, 1995, BK lent $5,000,000 to DS. After the loan is made, the balance in FP’s bank account remains with a range appropriate to meet FP’s working capital needs.

FP’s deposit with BK and BK’s loan to DS are financing transactions within the meaning of the regulations and together constitute a financing arrangement within the meaning of the regulations. Pursuant to Section 881(i), interest paid by BK to FP with respect to the bank deposit is exempt from withholding tax. Interest paid directly by DS to FP would not be exempt from withholding tax under Section 881(i) and therefore would be subject to a 30 percent withholding tax. Accordingly, there is a significant reduction in the tax imposed by Section 881, which is evidence of the existence of a tax avoidance plan. However, the director of field operations also will consider the fact that FP historically has maintained an account with BK to meet its working capital needs and that, prior to and after BK’s loan to DS, the balance within the account remains within a range appropriate to meet those business needs as evidence that the participation of BK in the FP-BK-DS financing arrangement is not pursuant to a tax avoidance plan. See Treas. Reg. Section 1.881-3(e), Example 20.

As pointed out in the above example, determining whether there is a significant reduction in tax as per the regulations, will require a careful analysis of all the facts and circumstances of the transaction at issue.

2. Did the Intermediate Entity Have Sufficient Available Money or Other Property of Its Own to Have Made the Advance to the Financed Entity?

The next factor in determining whether or not an intermediate entity is a conduit is to consider whether the entity “had sufficient available money or other property of its own to have made the advance of money or other property to it by the financing entity.” See Treas. Reg. Section 1.881-3(b)(2)(ii). If, just before the advance, the intermediate entity had on hand liquid assets at least equal to the principal amount of the advance, this presumably be a positive factor in the analysis. Also, liquid assets owned by a wholly owned subsidiary of the intermediate entity and easily accessed liquid assets would presumably constitute “available money or other property of [the intermediate entity’s] own.” See Tax Notes, Volume 146, Number 9, April 27, 2015, The Conduit Regulations Revisited, by Peter M. Daub.

3. Time Between Advances

The last factor in the determination of the existence of a tax avoidance plan is the time between the transactions. The regulations state as follows:

“The director of field operations will consider the length of the period of time that separates the advances of money or other property, or the grants of rights to use property, by the financing entity to the intermediate entity (in the case of multiple intermediate entities, from one intermediate entity to another), and ultimately by the intermediate entity to the financed entity. A short period of time is evidence of the existence of a tax avoidance plan while a long period of time is evidence that there is not a tax avoidance plan.” See Treas. Reg. Section 1.881-3(b)(2)(iii).

The regulations go on to state that a one-year lag between the first and last transaction of a conduit transaction can be considered “short” and can be considered evidence of a tax avoidance plan. For example, assume that on January 1, 1995, FP lends $10,000,000 to FS in exchange for a 10-year note that pays no interest annually. FS is obligated to pay $24,000,000 to FP. On January 1, 1996, FS lends $10,000 to DS in exchange for a 10-year note that pays interest annually at a rate of 10 percent per annum. The FS note held by FP and the DS note held by FS are financing transactions within the meaning of the regulations. Pursuant to the regulations, the short period of time (twelve months) between the loan by FP to FS and the loan by FS to DS is evidence that the participation of FS in the financing arrangement is pursuant to a tax avoidance plan. See Treas. Reg. Section 1.881-3(e), Example 17.

In analyzing whether an occasional short lag (or no lag) between the advance of FP to FS is evidence of a tax avoidance plan, one must bear in mind that the ultimate question is whether the involvement of DS is for a principal purpose of tax avoidance and if the transactions were deliberately timed to achieve a tax benefit.

Other Factors

In addition to the nonexclusive factors, the conduit regulations state that the IRS may consider other, unspecified factors in determining whether a tax avoidance plan exists. The examples in the conduit regulations suggest some unspecified factors. In Example 19, FP, a resident of a non-treaty country, issues debt in registered form that does not require the holder to issue a Form W-BEN. The purchasers of the debt are financial institutions and “there is no reason to believe that they would not furnish Forms W-8.” FP lends a portion of the debt proceeds to its U.S. subsidiary. The concludes by saying “because it is reasonable to assume that the purchasers of the FP debt would have provided certifications in order to avoid the withholding tax imposed by Section 881, there is not a tax avoidance plan. Accordingly, FP is not a conduit entity.” See Treas. Reg. Section 1.881-3(e), Example 19.

The example indicates that the existence of a reasonable assumption that the purchasers would have provided certifications establishes conclusively that there is no tax avoidance plan. Accordingly, although the determination of whether a tax avoidance plan exists depends on a consideration of all the facts and circumstances.

Example 20 of the conduit regulations illustrates another unspecific factor. According to Example 20 of the conduit regulations, over a period of years, FP has maintained a deposit with BK, a bank organized in the United States, that is unrelated to FP and its subsidiaries. FP often sells goods and purchases raw materials in the United States. FP opened the bank account with BK in order to facilitate this business and the amounts it maintains in the account are reasonably related to its dollar-denominated working capital needs. On January 1lends $5,000,000 to DS. After the loan is made, the balance in FP’s bank account remains within a range appropriate to meet FP’s working capital needs.

FP’s deposit with BK and BK’s loan to DS are financing transactions within the meaning of the regulations and together constitute a financing arrangement within the meaning of the regulations. Pursuant to Section 881(i), interest paid by BK to FP with respect to the bank deposit is exempt from withholding tax. Interest paid directly by DS to FP would not be exempt from withholding tax under Section 881(i) and therefore would be subject to a 30 percent withholding tax. Accordingly, there is a significant reduction in tax imposed by Section 881, which is evidence of the existence of a tax avoidance plan. However, the director of field operations also will consider the fact that FP historically has maintained an account with BK to meet its working capital needs and that, prior to and after BK’s loan to DS, the balance within the account remains within a range appropriate to meet those business needs as evidence that the participation of BK in the FP-BK-DS financing arrangement is not pursuant to a tax avoidance plan, all relevant facts will be taken into account.

Example 20 is helpful in that it suggests that the bank might not be a conduit entity even though it would not have made the loan to the subsidiary on substantially the same terms without the deposit. This is because, for an intermediate entity unrelated to both the financing entity and the financed entity to constitute a conduit, the intermediate entity’s financed entity could not have been on substantially the same terms without the financing from the entity. Thus, that the example even considers whether a tax avoidance plan exists logically must mean that the deposit favorably affects the loan terms.

The Rebuttable Presumption of Significant Financing Activities

The conduit regulations provide a rebuttable presumption that the participation of an intermediate entity in a financing arrangement is not under a tax avoidance plan if the intermediate entity is related to either or both the financing entity or the financed entity and the intermediate entity performs “significant financing activities” regarding the financing transactions forming part of the financing arrangement to which it is a party. See Tax Notes, Volume 146, Number 9, April 27, 2015, The Conduit Regulations Revisited, by Peter M. Daub. The performance of significant financing activities involves the satisfaction of several requirements:

1. The participation of the intermediate entity in the financing transactions produces efficiency savings by reducing transaction costs, overhead, and other fixed costs. See Treas. Reg. Section 1.881-3(b)(3)(ii)(B)(1).

2. The intermediate entity’s officers and employees participate actively and materially in arranging the intermediate entity’s participation in the financing transactions. See Treas. Reg. Section 1.881-3(b)(3)(ii)(B)(1).

3. In the country in which the intermediate entity is organized, its officers and employees manage and actively conduct the daily operations of the intermediate entity. Those operations must consist of a substantial trade or business or the supervision, administration, and financing for a substantial group of related persons. Any officer or employee of a related person cannot participate materially in these activities, other than to approve any guarantee of a financing transaction or to exercise general supervision and control over the policies of the intermediate entity. See Treas. Reg. Section 1.881-3(b)(3)(ii)(B)(2)(i).

4. In the country in which the intermediate entity is organized, its officers and employees actively and continuously manage material market risks arising from the financing transactions as an integral part of (a) the management of the intermediate entity’s financial and capital requirements (including management of risks of currency and interest rate fluctuations) and (b) the management of the intermediate entity’s short-term investments of working capital by entering into transactions with unrelated persons. Any officer or employee of a related person cannot participate materially in these activities, other than to approve any guarantee of a financing transaction or to exercise general supervision and control over the policies of the intermediate entity. See Treas. Reg. Section 1.881-3(b)(3)(ii)(B)(2)(ii).

A typical example of “significant financing activities” that satisfies requirements 1, 3, and 4 but not 2 can be found in Example 22 of the conduit financing regulations. The example states as follows:

FS is responsible for coordinating the financing of all of the subsidiaries of FP, which are engaged in substantial trades or businesses and are located in country T, country N, and the United States. FS maintains a centralized cash management accounting system for FP and its subsidiaries in which it records all intercompany payables and receivables; these payables and receivables ultimately are reduced to a single balance either due from or owing to FS and each of FP’s subsidiaries. FS is responsible for disbursing or receiving any cash payments required by transactions between its affiliates and unrelated parties. FS must borrow any cash necessary to meet those external obligations and invest any excess cash for the benefit of the FP group. FS enters into interest rate and foreign exchange contracts as necessary to manage the risks arising from mismatch in incoming and outgoing cash flows. The activities of FS are intended (and reasonably can be expected) to reduce transaction costs and overhead and other fixed costs. FS has 50 employees, including clerical and other back office personnel, located in country T. At the request of DS, on January 1, 1995, FS pays a supplier $1,000,000 for materials delivered to DS and charges DS an open account receivable for this amount. On February 3, 1995, FS reverses the account receivable from DS to FS when DS delivers to FP goods with a value of $1,000,000.

The accounts payable from DS to FS and from FS to other subsidiaries of FP constitute financing transactions within the meaning of the regulations and constitute a financing arrangement within the meaning of the regulations. FS’s activities constitute significant financing activities with respect to the financing transactions even though FS did not actively and materially participate in arranging the financing transactions because the financing transactions consisted of trade receivables and trade payables that were ordinary and necessary to carry on the trades or businesses of DS and the other subsidiaries of FP. Accordingly, FS’ participation in the financing arrangement is presumed not to be pursuant to a tax avoidance plan. See Treas. Reg. Section 1.881-3(e), Example 22.

In the next example in the conduit regulations, a U.S.-financed entity needs long-term financing to fund an acquisition of another U.S. company; the acquisition is scheduled to close on January 15, 1995. A non-U.S. affiliate entitled to benefits under its country’s treaty with the United States has a revolving credit agreement with a syndicate of banks located in a non-treaty country. On January 14, 1995, the affiliate, a U.S.-dollar-functional-currency business, borrows 10 billion yen for 10 years under a revolving credit agreement. The affiliate enters into a currency swap with an unrelated bank under which it eliminates its risk of fluctuations in the yen/dollar exchange rate over the entire 10-year term of its borrowing under the credit agreement. The next day, the U.S.-affiliate entity borrows $100 million from the non-U.S. affiliate for 10 years. This example concludes that since the affiliate has eliminated all material market risks arising from the financing transactions through its currency swap, the presumption does not apply. See Treas. Reg. Section 1.881-3(e), Example 23.

In another example found the anti conduit regulations, a non-U.S. affiliate in a treaty country borrows in deutsche marks for 10 years from its non-U.S. parent, which is not located in a treaty country. On January 1, 1995, FP lent FS DM 15,000,000 (worth $10,000,000) in exchange for a 10 year note that pays interest annually at a rate of 5 percent per annum. Also, on March 15, 1995, FS lends $10,000,000 to DS in exchange for a 10-year note that pays interest annually at a rate of 8 percent per annum. FS would have had sufficient funds to make the loan to DS without the loan from FP. FS does not enter into any long term hedging transactions with respect to these financing transactions, but manages the interest rate and currency risk arising from the transactions on a daily, weekly or quarterly basis by entering into forward currency contracts.

Because FS performs significant financing activities with respect to the financing transactions between FS, DS, and FP, the participation of FS in the financing arrangement is presumed not to be pursuant to a tax avoidance plan. The director of field operations may rebut this presumption by establishing that the participation of FS is pursuant to a tax avoidance plan, based on all the facts and circumstances. The mere fact that FS is a resident of country T is not sufficient to establish the existence of a tax avoidance plan. However, the existence of a plan can be inferred from other factors in addition to the fact that FS is a resident of country T. For example, the loans are made within a short time period and FS would not have been able to make the loan to DS without the loan from FP. See Treas. Reg. Section 1.881-3(e), Example 24.

Both Examples 23 and 24 involve long-term borrowers, as well as borrowing and on-loans that are precisely coordinated in timing and amount.See Tax Notes, Volume 146, Number 9, April 27, 2015, The Conduit Regulations Revisited, by Peter M. Daub. These examples are instructive in that they illustrate that the active and regular performance of risk management by intermediate entity management and employees will entitle a structure to the benefit of a rebuttable presumption that the participation of an intermediate entity in a financing arrangement is not under a tax avoidance plan.

Conclusion

The conduit regulations are extremely difficult to apply in the context of multinational financing transactions. Attempting to plan in this area is made even more difficult by the lack of updated examples in the conduit regulations. One would have hoped that with the promulgation of the proposed conduit regulations, the IRS or Treasury would have updated the examples in the conduit regulations and issued examples which discuss hybrid instruments. Perhaps, the IRS and Treasury will issue updated examples when the conduit regulations are finalized. Until the IRS and Treasury update the conduit regulation examples, practitioners will need to rely on the outdated examples in the conduit regulations when planning for the anti-conduit rules.

Anthony Diosdi is a partner and attorney at Diosdi Ching & Liu, LLP, located in San Francisco, California. Diosdi Ching & Liu, LLP also has offices in Pleasanton, California and Fort Lauderdale, Florida. Anthony Diosdi advises clients in tax matters domestically and internationally throughout the United States, Asia, Europe, Australia, Canada, and South America. Anthony Diosdi may be reached at (415) 318-3990 or by email: adiosdi@sftaxcounsel.com.

This article is not legal or tax advice. If you are in need of legal or tax advice, you should immediately consult a licensed attorney.