This article provides an overview of the rules governing outbound forward triangular mergers. This article uses a hypothetical Singapore corporation which acquires a U.S. corporation to discuss the issues commonly faced by tax professionals in outbound forward triangular merger. A forward triangular reorganization occurs when an acquiror uses the shares of its parent as merger consideration when the target merges into the acquiror, resulting in the acquiror receiving substantially all of the target’s assets.

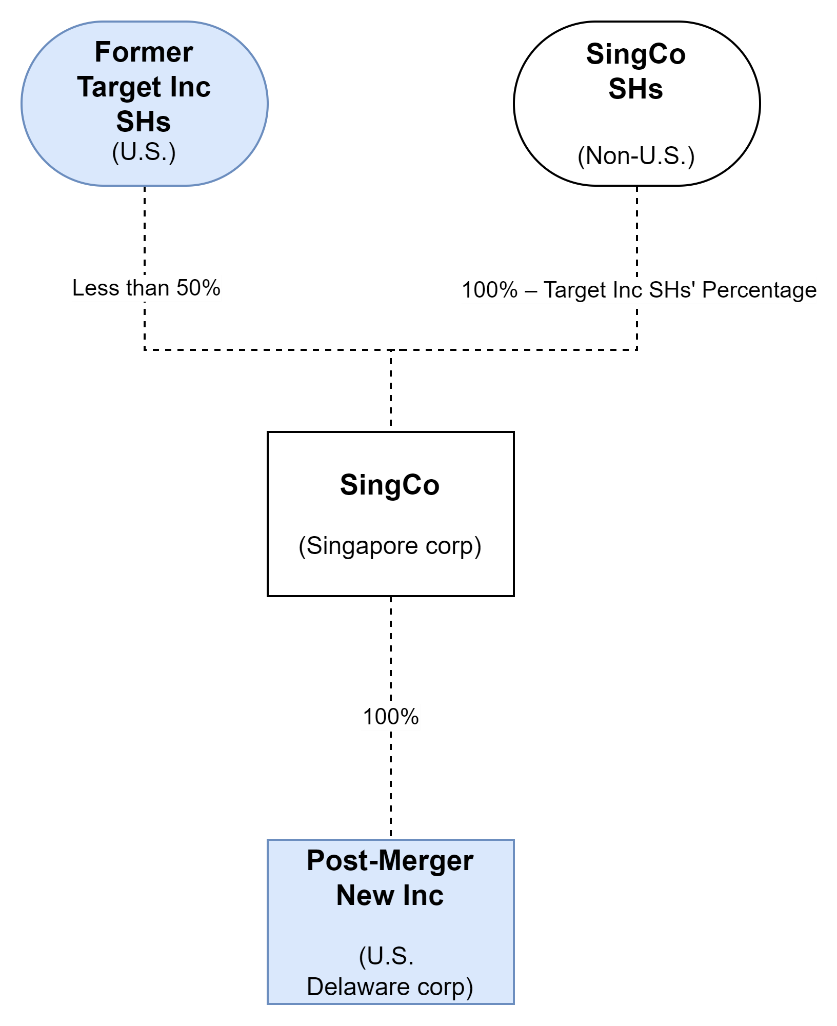

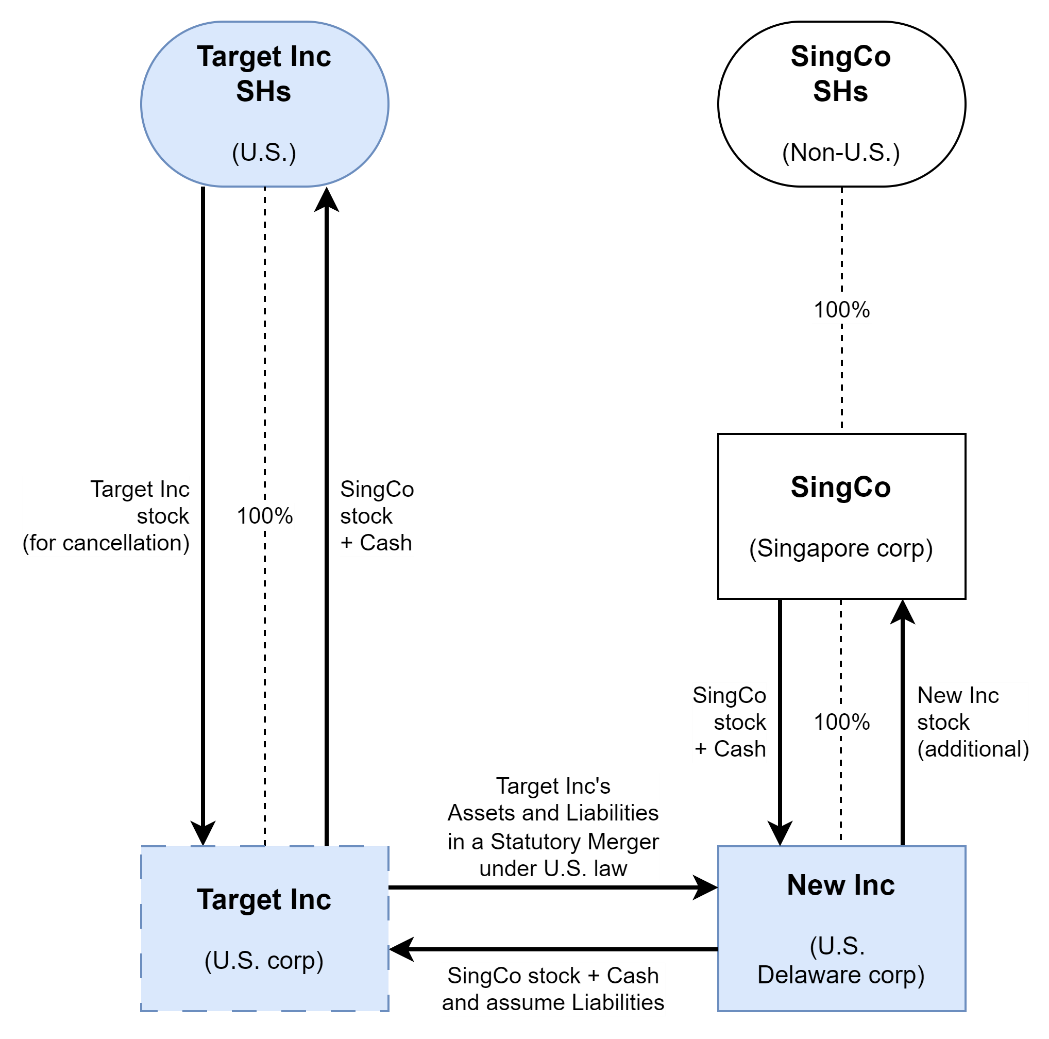

Let’s assume that a Singaporean corporation (“SingCo”) is entering into a forward triangular merger and for that it is setting up a new Delaware entity as NewCo with the purpose of acquiring business of the target corporation as TargetCo. The consideration is in the form of shares (50 percent) and the balance will be paid in cash.

Below, please see Illustration 1, which outlines the transaction.

Overview of the U.S. Tax Law Governing Outbound Forward Triangular Reorganizations

If a U.S. corporation is liquidated and its assets are distributed to foreign shareholders, U.S. tax will be imposed on the gain realized by the distributing corporation, except to the extent that a tax free-free-exchange provision provides otherwise. If the stock or assets of a U.S. corporation are acquired by a foreign corporation in exchange for stock of the foreign corporation, except to the extent that the gain is sheltered by a tax-free-exchange provision. Section 367 of the Internal Revenue Code requires a U.S. person transferring appreciated property to a foreign corporation to recognize a gain on the transfer. This result is achieved by denying corporate status to the foreign corporation, in which case the general rules for taxable exchanges apply.

The Internal Revenue Code provides for nonrecognition of gain or loss realized in connection with a considerable number of corporate organizational changes. These include acquisitive and other reorganizations defined in Section 368(a)(1) and divisive reorganizations under Section 355. Reorganizations, as defined in Section 368(a)(1), include statutory mergers and consolidations, acquisitions by one corporation of the stock or assets of another corporation, recapitalizations, and changes in form or place of organization.

The purpose of the reorganization provisions is to permit on a tax-free basis “such readjustments of corporate structures made in one of the particular ways specified in the [Internal Revenue] Code, as are required by business exigencies and which effect only a readjustment of continuing interest in property under modified corporate forms.” See Treas. Reg. Section 1.368-1(b). There are three general requirements for a transaction to qualify as a tax-free reorganization:

1 The transaction must have a business purpose.

2 The original owners must retain a continued proprietary interest in the reorganized corporation (the “continuity of interest” requirement). See Treas. Reg. Section 1.368-1(e). The Treasury Regulations consider the continuity of interest requirement satisfied if, following the transaction, historic shareholders of the target corporation hold stock of the acquiring corporation (as a result of prior ownership of target stock) representing 40% of the value of the stock of the target corporation. See Treas. Reg. Section 1.368-1(e)(2)(v), Ex. 1.

3 In an acquisitive reorganization, the acquiring corporation must either continue the acquired corporation’s historic business or use a significant portion of the acquired corporation’s historic business assets in a business (the “continuity of business enterprise” requirement). See Treas. Reg. Section 1.368-1(d). Under this rule, the acquirer must either continue the target’s historical business or use a significant portion of the target’s assets in an existing business for 2 years after the transaction.

The basic types of acquisitive reorganizations are:

1. A statutory Type A reorganization where one corporation (the acquiring corporation) acquires the assets and assumes the liabilities of another corporation (the target corporation) in a merger or consolidation effected under U.S. (or non-U.S.) law;

2. A Type B reorganization where the acquiring corporation exchanges its shares for the shares of the target corporation; and

3. A Type C reorganization where the acquiring corporation exchanges its shares for the assets of the target corporation.

A transaction that fails to qualify as one of the above discussed acquisitive reorganizations generally results in a taxable transaction.

Even if a transaction qualifies as a Type A, B, or C reorganization under Section 368(a)(1), any gains realized on the transaction may still be recognized (and thus taxable) under Section 367(a)(1) if a U.S. person transfers property to a foreign corporation. In the case of outbound transfers of shares in a U.S. corporation (the U.S. target company), the regulations provide for a limited-interest exception. This limited-interest exception generally provides for the nonrecognition of gain on the transfer of U.S. shares by a U.S. person to the transferee foreign corporation if all of the following tests are satisfied:

1. The U.S. person owns less than 5 percent (by both vote and value) of the stock of the transferee foreign corporation immediately after the transfer. Otherwise, the U.S. person must enter into a five-year gain recognition agreement with the Internal Revenue Service (“IRS”).

2. Fifty percent or less (by both vote and value) of the stock of the transferee foreign corporation is received, in the aggregate, by U.S. persons in the transaction.

3 Immediately after the transfer, fifty percent or less (by both vote and value) of the stock of the transferee foreign corporation is owned, in the aggregate, by U.S. persons who (i) are officers or directors of the U.S. target company or (ii) owned 5 percent or more (by vote and value) of the stock of the U.S. target company immediately before the transfer.

4. Satisfaction of the active trade or business test, which requires that (i) for the 36-month period immediately before the transfer, the transferee foreign corporation was engaged in an active trade or business outside the United States, (ii) at the time of the transfer, neither the U.S. persons nor the transferee foreign corporation intend to substantially dispose of, or discontinue, such trade or business, and (iii) at the time of the transfer, the value of the transferee foreign corporation is at least equal to the value of the U.S. target company. An active trade or business generally does not include the making or managing of investments for the account of the transferee foreign corporation.

See Treas. Reg. Section 1.367(a)-3(c)(1).

In the context of international corporate acquisitions, tax-free statutory mergers often take the form of forward triangular mergers or reorganizations, in which the acquiror uses the shares of its parent as the target merges into the acquiror, resulting in the acquiror receiving substantially all of the target’s assets. In order to qualify as a forward triangular merger, the transaction must qualify as a Type A reorganization.

Does the Consideration of 50 Percent and the Balance in Cash Qualify for a Forward Triangular Reorganization?

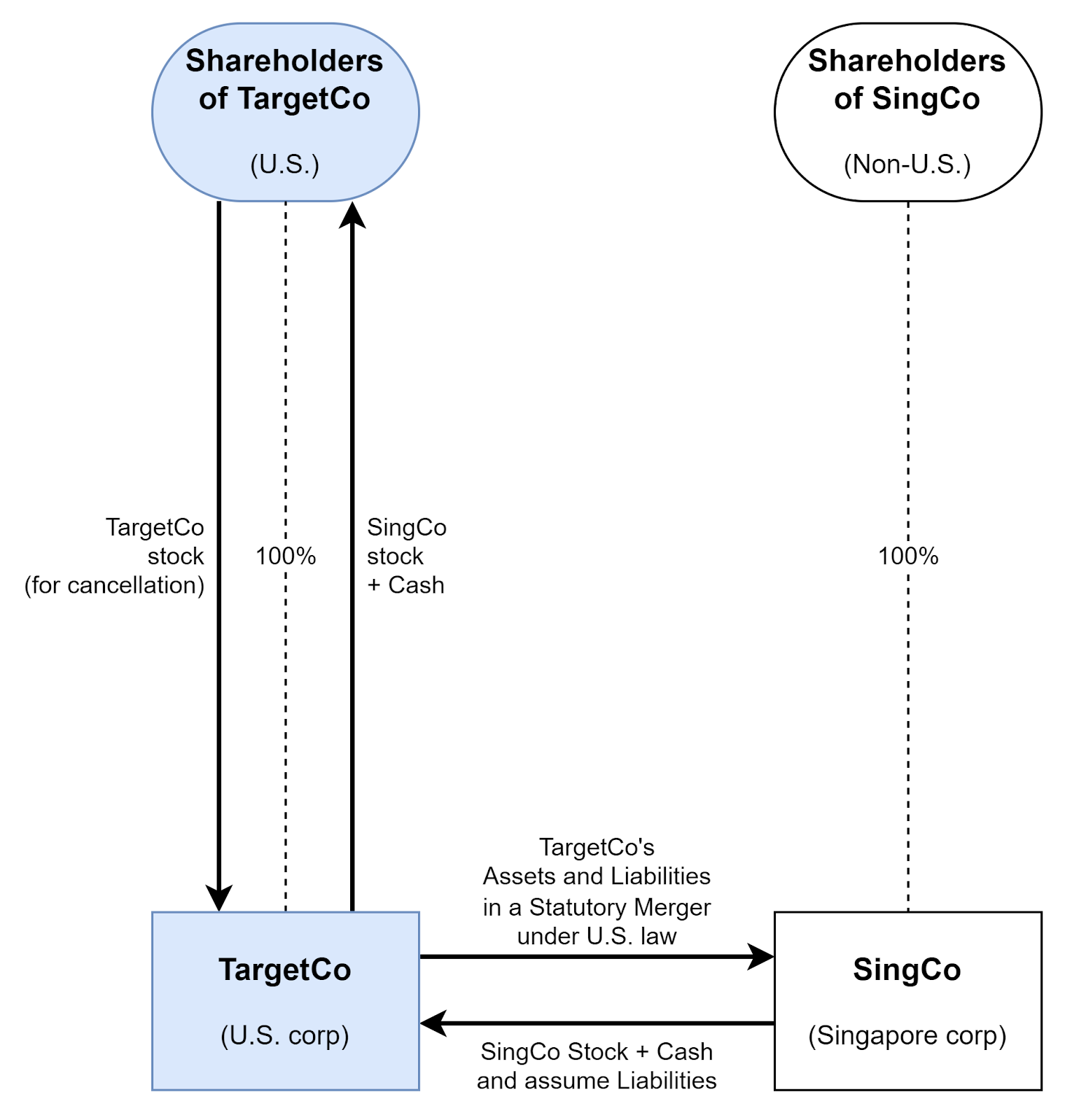

As provided in regulations to Internal Revenue Code Section 368(a)(2)(D), one of the requirements for a forward triangular merger is that the merger must be able to qualify as a Type A reorganization if the target corporation (TargetCo) were to merge directly into the controlling corporation (SingCo) instead of the acquiring corporation (NewCo). Below, as discussed in Illustration 2, is how a hypothetical Type A reorganization would be:

As a general matter, the “continuity of interest” requirement for a forward triangular Type A reorganization would be satisfied if at least 40% of the total consideration received consists of SingCo stock (though courts have allowed lower percentages). However, the non-stock consideration received by TargetCo’s shareholders would be treated as “boot” (non-like-kind property in an exchange and subject to tax) under Internal Revenue Code Section 356(a).

Does Treasury Regulation Section 1.367(a)-3(d) Treat the Transaction as an Indirect Stock Transfer?

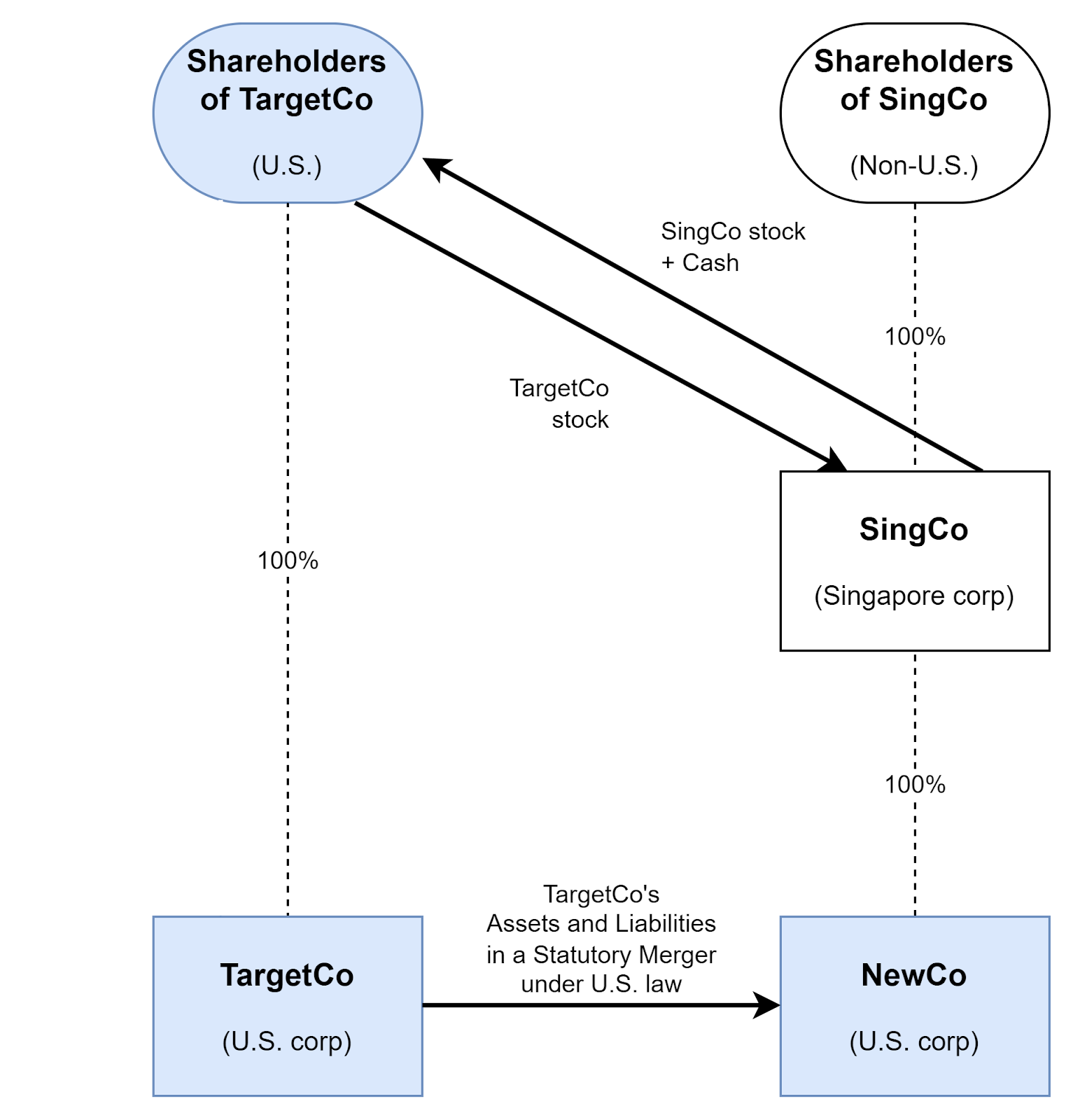

It is likely that paragraph (d) of Treasury Regulation Section 1.367(a)-3 would treat the transaction as an “indirect stock transfer” falling under paragraph (d)(1)(i), with facts similar to those in Example 1 of paragraph (d)(3) (where both the acquired and acquiring corporations are domestic). Accordingly, the transaction reformulated as an indirect transfer would be as follows:

In Example 1, the acquiring corporation “NewCo” (i.e., NewCo in the instant transaction) is a wholly-owned U.S. subsidiary of the foreign transferee corporation “F” (i.e., SingCo), and the acquired corporation “W” (i.e., TargetCo) is a wholly-owned U.S. subsidiary of a single U.S. corporate shareholder “A” (i.e., the shareholders of TargetCo). It should be noted that Example 1 includes the following additional facts:

1. Before the transaction, A and W filed a consolidated federal income tax return, and A did not own any stock in F (applying the attribution rules of Section 318, as modified by Section 958(b)).

2. In the transaction, A receives 40% of the stock of F — i.e., A does not receive more than 50% (by vote or value) of the stock of F.

If Example 1 applies, then the requirements of paragraph (c)(1) discussed above must be complied with in order to avoid gain recognition under Section 367(a)(1).

What are the Gain Recognition Agreements That May Need to be Executed by U.S. Transferees of TargetCo Stock?

Indirect stock transfers falling under paragraph (d)(1)(i) require the execution of five-year gain recognition agreements (as described in Treasury Regulation Section 1.367(a)-8) provided that, among other requirements, TargetCo shareholders who are U.S. persons do not receive in the aggregate more than 50% (by vote or value) of the stock of SingCo. See Treas. Reg. Section 1.367(a)-3(c)(1). A gain recognition agreement is an agreement with the IRS that would need to be signed by each TargetCo shareholder who is a U.S. person owning 5% or more (by vote and value) of the stock of SingCo. The terms of the agreement generally provide that if a triggering event (that is not otherwise excepted) occurs at any time during the gain recognition agreement term (“GRA term”), the U.S. transferor must include in income the gain that was realized but not recognized due to the gain recognition agreement. “GRA term” is defined as the period beginning on the date of the initial transfer and ending as of the close of the fifth full taxable year (not less than 60 months) following the close of the taxable year in which the initial transfer occurs. See Treas. Reg. Section 1.367(a)-8(c)(1)(i). The triggering events are specified in Treasury Regulation Section 1.367(a)-8(j), with the exceptions specified in Treasury Regulation Section 1.367(a)-8(k). Triggering events include, among others:

1. A disposition of substantially all of the assets of the transferred corporation (i.e., NewCo’s assets).

2. A disposition of stock of the transferee foreign corporation (i.e., SingCo stock).

The Limited Exception Rule

As indicated above, the regulations recognize that when an outbound transfer of shares occurs and the owners of the U.S. corporation whose shares are transferred are minority shareholders, the Section 367 “toll charge” tax should not apply because there is little chance of abuse.

For example, suppose Bob, a U.S. citizen wholly owns and is the only officer of Uncle Sam Corp, a U.S. corporation. In what would otherwise constitute a tax-free share-for-share transaction, Bob exchanges 100% of his shares of Uncle Sam for 3% of the voting shares of Prince Andrew, a United KIngdom Corporation. Bob, who wants to stay in the same business of Uncle Sam, may potentially not recognize gain as a result of satisfying the limited-interest exception if the following applies:

1) Bob receives less than 50% of Prince Andrew (only 3%);

2) As the only shareholder, officer or 50% shareholder of Uncle Sam, Bob does not own more than 50% of Prince Andrew, immediately after the transfer (Bob only owns 3%);

3) Prince Andrew must have operated for more than 36 months and neither Bob nor Prince Andrew will intend to discontinue Price Andrew’s business;

Going back to the examples discussed above, let’s assume that each shareholder in Target Inc will own (directly and indirectly) less than 5% (by vote and value) of the total outstanding shares of SingCo and, thus, they will not be required to enter into a GRA with the IRS. See Illustration 3 below:

The question is, does Treasury Regulation Section 1.367(a)-3(d)(3)(vi)(D)(2) apply to sales sold by an individual that qualified under the limited-interest exception. This provision, if applicable, would prohibit the sale or other disposition of New Inc stock for at least a two-year period. This particular provision appears under paragraph (d)(2)(vi) of the regulation, which sets forth in clause (A) of such paragraph a special rule, commonly referred to as the “coordination rule,” applicable to indirect stock transfers.

The coordination rule generally provides that if, pursuant to an indirect stock transfer described in paragraph (d)(1) of the regulation, a U.S. person transfers (or is deemed to transfer) assets to a foreign corporation in exchange described in Internal Revenue Code Section 351 or 361, then such transfer would be subject to the outbound toll charge imposed by Internal Revenue Code Section 367(a) or (b), as the case may be, prior to the application of the indirect stock transfer rules of Treasury Regulation Section 1.367(a)-3(d).

The coordination rule is subject to two exceptions. The first exception applies to transactions in which a U.S. corporation transfers assets to a foreign corporation then re-transfers or contributes assets to a foreign corporation in an Internal Revenue Code Section 351 exchange, and the foreign corporation then re-transfers or re-contributes those assets to another U.S. corporation in a subsequent or successive Section 351 exchange. See Treas. Reg. Section 1.367(a)(d)(2)(vi)(B)(2).

Leaving aside for now the question of whether the coordination rule even applies to the above discussed reorganization, the two-year restriction does not appear in the context of the second exception.

One of the requirements that must be satisfied for the first exception (such that the coordination rules does not apply to impose an outbound toll charge under Internal Revenue Code Section 367(a) or (d) prior to the application of the indirect stock transfer rules) is the inclusion of a statement in the U.S. income tax return of the domestic acquired corporation. In this statement, entitled “Required Statement under Section 1.367(a)3(d) for Assets Transferred to a Domestic Corporation,” officers of both the domestic acquired corporation and the foreign acquired corporation must certify that “if the foreign acquiring corporation of any stock of the domestic controlled corporation in a transaction described in paragraph (d)(2)(vi)(D) of [Treas. Reg. 1.367(a)-3], the domestic acquired corporation shall recognize gain as described in paragraph (d)(2)(vi)(E) of [Treas. Reg. 1.367(a)-3].”

A transaction described in paragraph (d)(2)(vi)(D) (which is subject to gain recognition under paragraph (d)(2)(vi)(E)) is one “where a principal purpose of the transfer by the domestic acquired corporation is the avoidance of U.S. tax that would have been imposed on the domestic acquired corporation on the disposition of the retransferred assets.”

Paragraph (d)(2)(vi)(D) provides for the following three scenarios:

1. A transaction is deemed to have the principal purpose of tax avoidance if the foreign acquiring corporation disposes of any stock of the domestic controlled corporation within two years of the transfer described in paragraph (d)(2)(vi)(A).

2. A transaction does not have a principal purpose of tax avoidance if the domestic acquired corporation (or the foreign acquired corporation on its behalf) demonstrates to the IRS’s satisfaction that this is indeed the case.

3. A transaction is deemed not to have the principal purpose of tax avoidance if the foreign acquiring corporation disposes of stock of the domestic corporation disposes of the stock of the domestic controlled corporation more than five years after the transfer described in paragraph (d)(2)(vi)(A).

The first and third scenarios above expressly apply to dispositions of the stock of a “domestic controlled corporation.” In order for there to be a “controlled asset transfer.” Treasury Regulation Section 1.367(a)-3(d)(1) defines this term as follows:

For purposes of this paragraph (d), if a corporation acquiring assets in an asset reorganization transfers all or a portion of such assets to a corporation controlled (within the meaning Internal Revenue Code Section 368(c) by the acquiring corporation as part of the same transaction, the subsequent transfer of assets to the controlled corporation will be referred to as a controlled asset transfer. See IRC Section 368(a)(2)(C).

In the reorganization discussed above, no such transfer is included in the overall transaction. In order for there to be one, an additional transfer would be required. In this case, New Inc (i.e., the corporation acquiring assets in the asset reorganization) would need to transfer all or part of Target Inc’s assets to another U.S. subsidiary that is directly or indirectly controlled by SingCo. No such additional step exists in the reorganization. Turning back to the coordination rule itself, we note that the rule comes into play only when assets are transferred by a U.S. person to a foreign corporation. Here, no such transfer occurs between the Target Inc and SingCo. Target Inc merges into New Inc, not SingCo.

The only possible way in which the coordination rule might apply to the reorganization discussed above would be where hypothetical straight A reorganization (as required to be considered by Internal Revenue Code Section 368(a)(2)(D)) were to constitute a “deemed” transfer of assets by Target Inc to SingCo within the meaning of the coordination rule. It appears that a hypothetical straight A reorganization is not intended to be considered in connection within the coordination rule. The hypothetical straight A reorganization is required by Internal Revenue Code Section 368(a)(2)(D) as a condition to qualify the actual forward triangular merger as a reorganization under Section 368(a)(1)(A). It is not the actual transaction to be entered into by the parties. Moreover, we note that the facts in the reorganization discussed above are similar to those of Example 1 of Treasury Regulation Section 1.367(a)-3(d)(3)(where both the acquired and acquiring corporations are domestic).

Example 1 makes no reference to the coordination rule and does not analyze a hypothetical straight A reorganization alongside the forward triangular merger presented in the example. Indeed, all the examples that are provided with respect to the coordination rule (i.e., Examples 6B, 6C, 9, 13) deal with either (i) a reorganization under Internal Revenue Code Section 368(a)(1)(C), followed by one or more controlled asset transfers or (ii) a transaction involving successive Section 351 exchanges. Accordingly, we do not believe that Treasury Regulation Section 1.367(a)-3(d)(2)(vi)(D)(2) applies to the reorganization discussed above.

Conclusion

With the expansion of cross-border transactions, more U.S. businesses will need to become familiar with U.S. tax, withholding, and compliance rules. Failure to become familiar with these rules can result in substantial penalties.

Anthony Diosdi is an international tax attorney at Diosdi & Liu, LLP. Anthony focuses his practice on providing tax planning domestic and international tax planning for multinational companies, closely held businesses, and individuals. In addition to providing tax planning advice, Anthony Diosdi frequently represents taxpayers nationally in controversies before the Internal Revenue Service, United States Tax Court, United States Court of Federal Claims, Federal District Courts, and the Circuit Courts of Appeal. In addition, Anthony Diosdi has written numerous articles on international tax planning and frequently provides continuing educational programs to tax professionals. Anthony Diosdi is a member of the California and Florida bars. He can be reached at 415-318-3990 or adiosdi@sftaxcounsel.com.

This article is not legal or tax advice. If you are in need of legal or tax advice, you should immediately consult a licensed attorney.