By Anthony Diosdi

The Tax Cuts and Jobs Act introduced two new Internal Revenue Code provisions targeting “hybrid arrangements.” The new Internal Revenue Code provisions include Section 245A(e), which denies a dividend received deduction under Section 245A with respect to hybrid dividends, and Section 267A, which denies certain interest or royalty deductions from hybrid transactions or hybrid entities. A hybrid arrangement generally seeks to exploit the differences in the tax treatment of a transaction or entity under the laws of two or more countries to secure double deductions, double exclusion from tax, or other tax benefits. The Tax Cuts and Jobs Act amendments to the Internal Revenue Code was a direct response to Action 2 of the Organization for Economic Co-operation and Development (“OECD”) Base Erosion and Profit Shifting (“BEPS”) Project that addressed hybrid and branch mismatch arrangements.

On April 7, 2020, the Internal Revenue Service (“IRS”) and the Department of Treasury (“Treasury”) issued final and proposed regulations regarding certain hybrid arrangements or entities that U.S. and foreign law characterize differently for tax purposes. The final regulations embrace the overall structure and approach of the proposed regulations which were promulgated in December of 2018.

Section 267A

Internal Revenue Code Section 267A disallows a deduction for interest or royalties paid or accrued in certain transactions involving a hybrid instrument. This provision of the Internal Revenue Code was designed to address cases in which a taxpayer is permitted a deduction under U.S. federal tax law, but the taxpayer does not have a corresponding income inclusion under foreign tax law. This is known as a “deduction/no-inclusion” (“D/NI”) outcome.

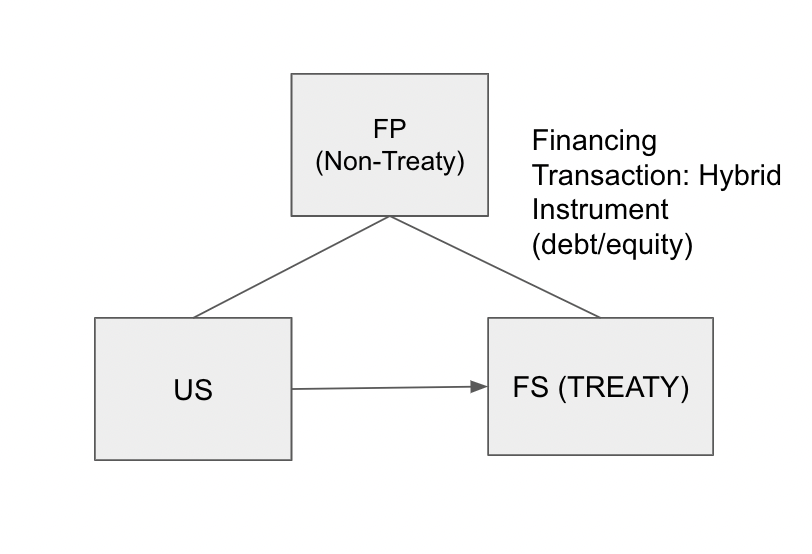

Below, please see Illustration 1 and Illustration 2 which demonstrates two examples of hybrid instruments.

Illustration 1.

FX incorporated in Country Y and wholly owns USCO, a United States corporation. FX executed a hybrid loan instrument with USCO. USCO paid FX $100 in interest payments.The hybris loan instrument classifies the interest payments as dividends in Country Y. Country Y does not tax foreign dividends. Thus, the $100 interest payment from USCO is not subject to tax in FX’s jurisdiction. Instead, in FX’s country, the $100 interest payment is treated as an excludable dividend for income tax purposes. The specified payment $100 payment will be treated as a “disqualified hybrid amount” (“DHA”) for U.S. tax purposes and the $100 interest payment is a non-deductible DHA.

Illustration 2.

Assume the facts for illustration 2 are the same as illustration 1. However, in this example, Country Y is taxed under a territorial regime which results in neither foreign source dividends nor foreign source interest being taxed. Since Country Y excludes the $100 specified payment (either as an interest or dividend) from taxation under its pure territorial taxing regime, the $100 the payment is not treated as a DHA. However, the $100 payment is not deductible per Treasury Regulation 1.267A-2(a)(1)(ii).

Background

The Proposed Regulation discusses the circumstances in which a deduction is disallowed under Section 267A. According to the Proposed Regulations, a “specified party’s” deduction for any interest or royalty paid or accrued (an amount paid or accrued with respect to the specified party for a “specified payment”) is disallowed to the extent it produces a D/NI outcome such as: 1) a “disqualified hybrid amount;” 2) a “disqualified imported mismatch amount;” and 3) payments that satisfy the requirements of the Section 267A anti-avoidance rule. These rules do not apply if the amount of a specified party’s interest and royalty deductions are less than $50,000.

The above discussed rules only apply to a “specified party.” A “specified party” is defined as any one of the following: a “tax resident” of the United States; a controlling foreign corporation (unless it has no U.S. shareholder that owns, within the meaning of Section 958(a), at least 10 percent of its stock (by vote or value)); or a “U.S. taxable branch.” See Treas. Reg. Section 1.267A-5(a)(17).

Hybrid Transactions

Long Term Deferral

The 2018 Proposed Regulations disallowed a deduction for any specified payment to the extent that the specified payment produced a D/NI outcome as a result of a hybrid branch arrangement. Several provisions of the 2018 Proposed Regulations addressed long-term deferral, which results when there is deferral beyond a taxable period ending more than 36 months after the end of the specified party’s taxable year. The final regulations retained the long-term deferral provisions but provided that a determination as to whether long-term deferral exists is made by establishing when the payment is “reasonably expected” to be included in income. This is discerned at the time the payment is made. The regulations also state that if a specified payment will never be recognized under the tax law of the specified recipient (the foreign tax law does not impose an income tax) the long-term deferral rule does not apply.

Hybrid Sale/License

In response to certain comments on the definition of hybrid transactions, the Final Regulations added a rule exempting hybrid sale/license transactions from the hybrid transaction rule. A hybrid sale/license transaction could occur, for example, when a specified payment is treated as royalty for U.S. tax purposes, and a contingent payment of consideration for the purpose of intangible property under the tax law of a specified recipient.

Below, please see Illustration 3 which discusses a hybrid sales/license transaction.

Illustration 3.

FCo is a CFC incorporated in Country Z. USCo, a corporation incorporated in the United States. USCo wholly owns FCo. Assume that FCo sells intellectual property to USCo. However, FCo does not transfer “all substantial rights” to the IP to USCo. USCo agreed to make annual payments for the use of intellectual property transferred to it from FCo. FCo is permitted to treat the transfer of intellectual property to USCo as an installment sale under the tax laws of Country Z. In addition, FCo is permitted to recover its basis in its intellectual property first. For U.S. tax purposes, USCo treats the payments to FCo as deductible royalties. The final anti-hybrid rules permit such a transaction.

Interest-Free Loans

Under the Final Regulations, payments under interest free loans and similar arrangements are deemed to be made under a hybrid transaction to the extent that a payment is imputed (under Internal Revenue Code Sections 482 or 7872) and the tax resident or taxable branch to which the payment is made does not take the payment into account under its tax law because that tax law does not impute interest. An interest free loan includes an instrument that is treated as debt under both U.S. tax law and the holder’s tax law but provides no stated interest. Such an instrument would give rise to a D/NI outcome to the extent the issuer is allowed an imputed deduction, but the holder is not required to impute interest income.

Below, please see Illustration 4 which discusses an interest free-free hybrid transaction.

Illustration 4.

Assume that USCo borrows from F1 (Country X) under a normal loan, treated as best both in the United States and in Country X. F-1 borrows from F2 (Country Y). This loan is also debt in both Country X and Y, but the loan is interest-free. F-1 is allowed an imputed interest deduction under Country X tax laws. However, F-2 is not required to impute interest income under Country Y-s tax laws. In this case, interest free loans are treated as hybrid transactions under Treasury Regulation Section 1.267A-2(a)(4) and the interest paid by USCo to F-1 is treated as a disqualified hybrid mismatch amount. See Baker McKenzie, Tax News and Developments, North America, Final Anti-Hybrid Rules, Jeff Rubinger and Summer Ayers LePree.

Disregarded Payments

Dual Inclusion Income

The 2018 Proposed Regulations provide that a deduction for a disregarded payment is disallowed to the extent that it exceeds the specified party’s “dual inclusion income.” Dual inclusion income is defined by these rules as income included in both the income of the specified party and the tax resident or branch to which the payment is provided. In response to comments, Treasury and the IRS concluded in the final Section 267A regulations that an item of income of a specified party should be dual inclusion income even though, by reason of a participation exemption or other relief particular to a dividend, the item is not included in the income of the tax resident or taxable branch to which the disregarded payment is made, provided that the application of the participation exemption or other relief relieves double-taxation. See Treas. Reg. Section 1.267A-2(b)(3)(ii); Treas. Reg. Section 1.267A-6(c)(3)(iv). The final Section 267A regulations provide an identical rule in situations in which an item of income of a specified party is included in the income of the tax resident or branch to which the disregarded payment is made. However, the amount is not included in the income of the specified party by reason of a dividends received deduction.

Exception for Payments Otherwise Taken Into Account Under Foreign Law

Under the 2018 Proposed Regulations, a special rule ensured that a specified payment was not a deemed branch payment to the extent that the payment was otherwise taken into account under the home office’s tax law in such a manner that there was no mismatch. The 2018 Proposed Regulations did not, however, provide a similar rule in analogous cases involving disregarded payments. To provide symmetry between the disregarded payment rule and the deemed branch payment rule, the final Section 267A regulations add to the disregarded payment rule a special rule similar to the special rule in the deemed branch payment context.

Allocation of Interest Expense to U.S. Taxable Branches

The 2018 Proposed Regulations provided that a U.S. taxable branch of a foreign corporation was considered to pay or accrue interest allocable under Section 882(c)(1) to effectively connected income of the U.S. taxable branch. According to the Treasury and IRS, these rules are necessary to determine whether a U.S. taxable branch specified payment was made pursuant to a hybrid or branch arrangement.

The 2018 Proposed Regulations did not, however, obtain rules for tracing a foreign corporation’s distributive share of interest expense when the foreign corporation was a partner in a partnership that had a U.S. asset or rules for tracing interest that was determined under the separate currency pools method. The final Section 267A regulations therefore provide that a U.S. taxable branch must use a direct tracing approach to identify the person to whom interest described in Treasury Regulation Section 1.882-5(a)(1)(ii) or Treasury Regulation Section 1.882-59e) is payable.

In addition, in order to avoid treating similarly situated taxpayers differently under Section 267A, the final Section 267A regulations provide that foreign corporations should use U.S. booked liabilities to identify the person to whom an interest expense is payable, without regard to which method the foreign corporation uses to determine its interest expense under Section 882(c)(1).

Reverse Hybrids

A reverse hybrid is an entity that is fiscally transparent under the tax law of the country in which it is established but not under the tax law of an investor of the entity. A reverse hybrid can present D/NI outcomes because it is not a tax resident in the country where it is established, and an investor is not considered to derive the payment under its home country’s tax law. A specified payment made to a reverse hybrid is generally a disqualified hybrid amount to the extent that an investor does not include the payment in income. Under the Final Regulations, an entity is fiscally transparent and a hybrid if under the tax law of the country where it is established if it is considered fiscally transparent under the definition of Treasury Regulation Section 1.894-1(d)(3)(ii) and (iii).

Current-Year Distributions from Reserve Hybrid

Under the 2018 Proposed Regulations, when a specified payment was made to a reverse hybrid, it generally was a disqualified hybrid amount to the extent that an investor did not include the payment in income. According to the preamble to the 2018 Proposed Regulations, although a subsequent distribution may have been included in the investor’s income, the distribution may not occur for an extended period and, when it did occur, it may have been difficult to determine whether the distribution was funded from an amount comprising the specified payment.

One comment to the 2018 Proposed Regulations noted that, if a reverse hybrid distributed all of its income during a taxable year, then current year distributions should have been taken into account for purposes of determining whether an investor of the reverse hybrid included in income a specified payment made to such reverse hybrid. The final Section 267A regulations provide that in these cases, a portion of a specified payment should relate to each of the current year distribution from the reverse hybrid. Treasury and the IRS have determined, however, that it would be too complex to take into account current year distributions in cases in which the reverse hybrid does not distribute all of its income during the taxable year. See Baker McKenzie, Tax News and Developments, North America, Final Anti-Hybrid Rules, Jeff Rubinger and Summer Ayers LePree.

Multiple Investors in a Reverse Hybrid

When an investor of a reverse hybrid owns only a portion of the hybrid’s interest and does not include in income its portion of a specified payment made to the reverse hybrid, the Final Regulations clarify that only the no-inclusion portion will give rise to a disqualified hybrid amount.

The preamble provides the following example to clarify this rule. Assume that a $100 specified payment is made to a reverse hybrid 60% of the interest of which are owned by a Country X investor (the tax law of which treats the reverse hybrid as not fiscally transparent) and 40% of the interests of which are owned by a Country Y investor (the tax law of which treats the reverse hybrid as fiscally transparent). If the Country X investor does not includes any portion of the payment in income, then $60 of the payment would generally be a disqualified hybrid amount under the reverse hybrid rule, calculated as $100 (the no-inclusion that actually occurs with respect to the Country X investor) less $40 (the non-inclusion that would occur with respect to the Country X investor absent hybridity).

Exceptions Relating to Disqualified Hybrid Amounts

1. Effect of Inclusion to Disqualified Hybrid Amounts

Under the 2018 Proposed Regulations, a specified payment generally would be a disqualified hybrid amount to the extent that a D/NI outcome occurs with respect to any foreign country as a result of a hybrid or branch arrangement, even if the payment is included in income in another country. Although commentators asked the Treasury to remove the provision, or address it through general anti-avoidance rules, the Final Regulations retain the approach of the 2018 Proposed Regulations. According to the Preamble, that approach prevents the routing of a specified payment through a low-tax third country to avoid Section 267A, as well as the use of a hybrid or branch arrangement to place a taxpayer in a better position than it would have been absent the arrangement.

2. Amounts Included or Includable in the United States

The Final Regulations revise the rule in the 2018 Proposed Regulations that would not treat a specified payment as a disqualified hybrid amount to the extent that it was included in the income of a tax resident of the United States or a U.S. taxable branch, or was taken into account by a U.S. shareholder under subpart F or GILTI rules. The determination of amounts considered taken into account under subpart F rules would be made without the earnings and profits limitation of Section 952. The Final Regulations also reduce the determination of amounts considered taken into account under GILTI to correspond with the reduced rates on GILTI inclusions resulting from the Section 250 deduction.

Below, please see Illustration 5 which demonstrates a payment by a reverse hybrid.

Illustration 5.

In this example interest paid to the Bank is potentially deductible in F Co’s home country and the United States. Here, U.S. Partnership is wholly owned by F Co. Typically, under the regulations, the U.S. Partnership would be “fiscally transparent.” Which basically means that the domestic entity’s tax items flow through to its owners under the entity’s or the interest holder’s jurisdiction. However, in certain cases, this tax treatment can be avoided if the foreign owned entity is treated as a U.S. partnership or disregarded entity. Since, U.S. Partnership is treated as a partnership for U.S. tax purposes, the current hybrid entity regulations may permit a double deduction outcome.

3. Disqualified Imported Mismatch Payments

The 2018 Proposed Regulations applied an “imported mismatch” rule to prevent the importation into the United States’ taxing jurisdiction of certain foreign hybrid arrangements through the use of non-hybrid arrangements. Generally, the imported mismatch rule of the 2018 Proposed Regulations disallowed deductions for specified payments to the extent that the payment was a “disqualified imported mismatch amount,” which was an imported mismatch amount such that the income attributable to the payment was directly or indirectly offset by a hybrid deduction. The general approach taken in the 2018 proposed regulations with respect to the imported mismatch rule has been retained by the treasury and the IRS. However, changes have been made to reduce complexity of this rule. The final regulations narrow the definition of an imported mismatch payment to provide that a specified payment is an imported mismatch to the extent it is neither a disqualified payment nor included in income in the United States.

Below, please see Illustration 6 which discusses a disqualified imported mismatch payment

Illustration 6.

Assume FY is a reverse hybrid because it is transparent for Country Y purposes and a regarded taxable entity for Country X purposes. Also assume that Country X does not tax FX on the specified payment under any anti-deferral taxing regime. As a result, the specified payment of $100 to FY is a DHA. This is because the interest payments are not subject to taxation in any foreign jurisdiction. As a result, the interest payment in the United States made to FY and FV are subject to 30 percent withholding tax. In addition, there are no treaty benefits available in this transaction. See Baker McKenzie, Tax News and Developments, North America, Final Anti-Hybrid Rules, Jeff Rubinger and Summer Ayers LePree.

Hybrid Deductions

An allowable deduction under a tax resident’s or taxable branch tax law is generally a hybrid deduction if the inclusion of rules are substantially similar to Treasury Regulation Sections 1.267A-1 through 1.267A-3 and 1.267A-5 in that tax law would result in the deduction’s disallowance. The Final Regulations clarify how this standard applies when the tax law of a tax resident or taxable branch contains hybrid mismatch rules. This list includes deductions for: 1) equity; 2) interest-free loans; and 3) amounts that are not included in the foreign country. See Treas. Reg. Section 1.267A-4(b)(2)(i). Consequently, if a tax resident is in a jurisdiction with hybrid mismatch rules, only these three deductions such be considered.

The final regulations also continue to treat Notional Interest Deductions (“NID”) as hybrid deductions in the context of imported mismatch, but only to the extent that they are permitted for a tax resident under its tax law for accounting periods beginning on or after December 20, 2018.

Hybrid Deductions of CFCs

Under the 2018 Proposed Regulations, only a tax resident or a taxable branch that was not a specified party may have a hybrid deduction and made a “funded taxable payment.” This approach was intended to prevent potential double taxation under Section 267A of specified payments involving CFCs, because payments made to CFCs would generally be includible in income in the United States, and payments by CFCs are subject to disallowance as disqualified hybrid amounts. To prevent the avoidance of the imported mismatch rule through the use of CFCs that are not wholly owned by U.S. tax residents, the final Section 267A regulations permit CFCs to incur hybrid deductions and make funded taxable payments. Furthermore, if a CFC’s disqualified hybrid amount is only partially owned by U.S. tax residents, only a portion of the disqualified hybrid amount disallows a CFC payment from giving rise to a hybrid deduction or a funded taxable payment, because as the preamble to the final Section 267A regulations points out, disallowing the CFC a deduction for the disqualified hybrid amount will only partially increase the U.S. tax base, if at all. A hybrid deduction directly or indirectly offsets the income attributable to an imported mismatch payment to the extent that the payment directly or indirectly funds the hybrid deduction. Furthermore, ordering rules apply to offset income against the hybrid deductions which will be discussed below.

Funded Taxable Payments

For an imported mismatch payment to fund a hybrid deduction, the imported mismatch payee must directly or indirectly make a “funded taxable payment” to the tax resident or taxable branch that incurs the hybrid deduction. Furthermore, the final Section 267A regulations provide that another foreign tax resident or foreign taxable branch includes the amount in income, as determined under Treasury Regulation Section 1.267A-3(a), by treating the amount as the specified payment.

Ordering Rules

The final Section 267A regulations include ordering rules for offsetting income attributable to an imported mismatch payment against a hybrid deduction. When there are multiple mismatch payments, a hybrid deduction is first considered to offset income attributable to the imported mismatch payment that has the closest nexus to the hybrid deduction. The Final Regulations retain this approach with two clarifications. First, the final Section 267A regulations apply a hybrid deduction to offset income that is attributable to a “factually-related imported mismatch payment.” A factually-related imported mismatch payment” is essentially the imported mismatch payment with the closest nexus to the hybrid deduction. In other words, an imported mismatch payment is a factually related mismatch only if a design of the plan or series or related transactions was for the hybrid deduction to offset income attributable to the payment. Second, to the extent there is any excess hybrid deduction remaining after applying the deduction to the factually related imported mismatch payment, that excess should offset an imported mismatch amount that is not a “factually related imported mismatch amount” and which directly funds the hybrid deduction.

Payer-Payee Relatedness

A hybrid deduction offsets income attributable to an imported mismatch payment only if the tax resident or taxable branch incurring the hybrid deduction is related to the imported mismatch payer. An important mismatch payment indirectly funds a hybrid deduction if the imported mismatch payee, as well as each intermediary tax resident or taxable branch, is related to the imported mismatch payer.

Below, please see Illustration 7 which provides an example of a disqualified imported mismatch amount.

Illustration 7.

Assume that the foreign parent excludes a hybrid dividend from income under a participation exemption. As a result, the interest payment by a U.S. payor is a disqualified imported mismatch amount to the extent income attributable to the payment is offset by a “hybrid deduction” incurred by foreign payee related to the U.S. Payor. A “hybrid deduction” arises here because the foreign imported mismatch payee is allowed a deduction under its tax law that would be a DHA under Treasury Reg. Section 1.267A-2 if its country had applicable U.S. rules. The interest paid by the U.S. Payor is therefore a disqualified imported mismatch amount and the U.S. deduction is disallowed. See Baker McKenzie, Tax News and Developments, North America, Final Anti-Hybrid Rules, Jeff Rubinger and Summer Ayers LePree.

Coordination with Foreign Mismatch Payments

1. Deemed Imported Mismatch Payments

The 2018 Proposed Regulations coordinate the U.S. imported mismatch rule with foreign imported mismatch rules through a special rule under which certain payments by non-specified parties were deemed to constitute imported mismatch payments. The deemed imported mismatch rule reduced the extent to which a payment of a specified party was treated as funding a hybrid deduction. The final Section 267A regulations modify the deemed imported mismatch rule so that it takes into account payments disallowed under a foreign imported mismatch rule, rather than payments for which a deduction is actually denied under the foreign imported mismatch rule.

2. Special Rules for Applying Imported Mismatch Rule

When the U.S. imported mismatch rule treats a deduction as a hybrid deduction, but a foreign imported mismatch rule does not, an inappropriate result may arise. Thus, the Final Regulations specify that the U.S. imported mismatch rule is first applied by taking into account only hybrid deductions that are unlikely to be treated as hybrid deductions for purposes of a foreign hybrid mismatch rule.

Anti-Avoidance Rule

The Section 267A anti-avoidance rule, as it appears in the final Section 267A regulations, disallows a specified party’s deduction for a specified payment to the extent that the payment satisfies the following conjunctive test:

1. The payment (or income attributable to the payment) is not included in the income of a tax resident or taxable branch under Treasury Regulation Section 1.267A-3(a); and

2. “A principal purpose of the terms or structure of the arrangement (including the form and the tax laws of the parties to the arrangement) is to avoid the application of the regulations in this part under Section 267A in a manner that is contrary to the purpose of Section 267A and its regulations in this part under Section 267A.”

With respect to the test’s first prong, Treasury Regulation Section 1.267A-3(a) provides the conditions for when a tax resident or taxable branch is treated as including a specified payment in income for the purposes of Section 267A. If a specified party makes a payment to a tax resident or taxable branch and the payments is not treated as included in income under Treasury Regulation Section 1.267A-3(a), that specified payment meets the first prong of the anti-avoidance conjunctive test. If that payment was structured or arranged with a principal purpose to avoid Section 267A, Section 267A disallows the corresponding U.S. deduction.

There are two ways by which a payment is not considered included in income under Treas Reg Section 1.267A-3(a). First, a specified payment is not considered included in income if the royalty or interest, for which there was a corresponding U.S. deduction, is not included in income under foreign law within 36 months after the end of the specified party’s taxable year. Said simply, this rule coupled with the anti-avoidance rule, disallows deductions for hybrid and branch arrangements resulting in long-term tax deferral.

Second, a specified payment is not included in income for purposes of Treasury Regulation Section 1.267A-3(a) if the payment is reduced or otherwise offset by “an exemption, exclusion, deduction, credit (other than for withholding tax imposed on the payment), or other similar relief particular to such type of payment. The regulations provide the following examples of such reductions or offsets: “1) participation exemption; 2) a dividends received deduction; 3) a deduction or exclusion with respect to a particular category of income (such as income attributable to a branch, or royalties under a patent box regime); 4) a credit for underlying taxes paid by a corporation from which a dividend is received; and 5) a recovery of basis with respect to stock or recovery of principal with respect to indebtedness.” Furthermore, a payment is not treated as reduced or offset for this purpose if it is offset by a “generally applicable deduction or other tax attribute, such as a deduction for depreciation or net operating loss.”

Section 245A(e)

Internal Revenue Code Section 245A(e) generally denies the dividends received deduction (the “DRD”) under Section 245A for hybrid dividends (i.e., amounts received from a CFC if the dividend gives rise to a local country deduction or other tax benefit). A hybrid dividend is an amount received from a CFC for which a Section 245A a CFC for which a Section 245A DRD would otherwise allow, and for which the CFC received a deduction or a tax benefit with respect to that income in a foreign country.

The 2018 Proposed Regulations provide rules for identifying and tacking hybrid dividends and set forth standards for identifying hybrid deductions.The 2018 Proposed Regulations detailed rules about what constituted a hybrid deduction, how to calculate and track hybrid deduction accounts, and how to determine a CFC made a hybrid dividend. The final Section 245(e) regulations keep much of these rules intact. However, some changes are made to the Proposed Regulations.

The final regulations provide that the determination of whether a relevant foreign tax law allows a deduction or other tax benefit is made without regard to the foreign hybrid mismatch rules, provided that the amount gives rise to a dividend for U.S. tax purposes or is reasonably expected for U.S. tax purposes to give rise to a dividend that will be paid within 12 months after the taxable period in which the deduction would otherwise be permitted. The regulations also state that deductions with respect to equity, like NIDs, are hybrid deductions regardless of whether the deductions result from an actual payment, accrual, or distribution.

The final Section 245(e) regulations retain most of the rules regarding the effect of transfers of stock on hybrid deduction accounts, but add some new rules. The new rules address Section 355 spin-off transactions, requiring taxpayers to allocate hybrid deduction accounts in the same manner as E&P. For mid-year transfers of stock, the final regulations generally allocate a hybrid deduction account between the seller and the buyer based on the number of days in the taxable year. In addition, the final rules add a new general anti-duplication rule that ensures that when foreign tax law deductions or other tax benefits are in effect duplicated at different tiers, the deductions only give rise to a hybrid deduction of the higher-tier CFC. Moreover, the regulations clarify that, in case of a Section 338(g) election, the shareholder of the “new target” does not succeed to the hybrid deduction account with respect to a share of the “old target.” See US IRS Proposes Regulations Implementing Anti-Hybrid Mismatch Rules and Expanding Scope of Dual Consolidated Loss Regulations, EY Global, Jan 4, 2019.

The 2018 Proposed Regulations also contained an anti-avoidance rule that requires adjustments to be made if a transaction or arrangement is engaged in with a principal purpose of avoiding the purpose of the regulations. The final Section 245(e) regulations retain this rule, but modify it to provide that the anti-avoidance rule does not apply to disregard a restructuring of a hybrid arrangement into a non-hybrid arrangement. Finally, to deal with an unintended result of the 2018 Proposed Regulations, the final regulations provide the tiered hybrid dividend rule only applies to a domestic corporation that is the U.S. shareholder of both the upper-tier and low-tier CFC and, thus, does not apply to individuals.

Below, please see Illustration 8, Illustration 9, and Illustration 10 which discuss tiered hybrid dividends, hybrid dividends, and the impact of the imputation systems.

Illustration 8.

In this example, there is accrued interest on hybrid debt between Holdco and Opco which gives rise to hybrid deductions to “hybrid deduction accounts” (“HDA”). An actual payment of interest/dividends is a hybrid dividend, which is subpart F income to Parent.

Illustration 9.

In this example, the shares of A and B are equally valued. During Year 1, under Country X tax laws, FX accrues $80x of interest with respect to Share A. FX is allowed a deduction. In year 2, FX distributes $30x on Share A and $30x on Share B. Both distributions are treated for U.S. tax purposes as a dividend eligible for the Section 245A DRD. See Treas. Reg. Section 245A(e)-1(g), Ex. 1(i).

Illustration 10.

FZ distributes a dividend to FX. Similar to Malta, Country Z allows a refundable credit to FX for 75 percent of the Z corporate tax paid for the earnings that funded the dividend to FX. As a result, FZ dividend is treated as a hybrid dividend for the amount of the dividend that interpolates to the tax effected credit (in this case 70% of the dividend). If FZ imposes withholding tax on the dividend, that reduces or eliminates the hybrid dividend to the extent it negates the refundable credit. See Baker McKenzie, Tax News and Developments, North America, Final Anti-Hybrid Rules, Jeff Rubinger and Summer Ayers LePree.

Proposed Section 245A(e) Regulations

Congress enacted Section 245A(e) to combat the double non-taxation effects of certain hybrid arrangements. However, when a U.S. shareholder has a subpart F or GILTI inclusion with respect to a CFC and Section 245A(e) provisions also apply, double taxation can result. To mitigate this concern, Treasury issued proposed regulations that allow for an adjustment to a CFC’s hybrid deduction account to the extent that the CFC’s hybrid deduction account to the extent that the CFC’s earnings are included in income under subpart F or GILTI rules. Rather than providing for a dollar-for-dollar reduction in the hybrid deduction account by the amount of the inclusion, the proposed rules require taxpayers to perform a complex calculation that takes into account the potential benefit of foreign tax credits and the Section 250 deduction.

The proposed regulations generally reduce a hybrid deduction account with respect to a share of stock of a CFC by an “adjusted subpart F inclusion” or an “adjusted GILTI inclusion” with respect to the share. This reduction, however, cannot exceed the hybrid deduction allocated to the share for the taxable year multiplied by the ratio of the subpart F income or tested income, as applicable, of the CFC to the CFC’s taxable income. The regulations also provide ordering rules for when adjustments are required under multiple provisions.

To calculate the adjusted subpart F inclusion, a taxpayer must first determine two amounts, on a share-by-share basis: 1) its pro rata share of the CFC’s subpart F income included in income in the taxpayer’s current year; and 2) the “associated foreign income taxes” with respect to that subpart F inclusion (determined by allocating foreign taxes to the subpart F income groups under Section 960 and the regulations thereunder). The following two step process must be followed. First, the taxpayer adds the pro rata share of the subpart F inclusion and associated foreign income taxes, which is intended to reflect the Section 78 gross-up. From that amount, the taxpayer then subtracts the quotient of the associated foreign income taxes divided by the corporate tax rate (21%), which is intended to equal the amount of income offset by the foreign taxes. Express formulatically:

Adjusted Subpart F Inclusion = Subpart F inclusion + Associated Foreign Income taxes

– Associated Foreign Income Taxes

0.21

The adjusted GILTI inclusion calculation follows a similar approach, but has three key differences. First, associated foreign income taxes are calculated by allocating foreign taxes to the tested income group and then multiplying by the taxpayer’s “inclusion percentage.” Second, after the first step, there is an interim step in which the taxpayer multiples the grossed-up inclusion by the difference between 100 and the percentage in Section 250(a)(1)(b) (currently at 50%). Third, in the final step, the taxpayer also multiplies the associated foreign income taxes by 80% to account for the GILTI reduction for foreign tax credits. Expressed formulaically:

Adjusted GILTI Inclusion = ((GILTI + Associated Foreign Income Taxes) x 0.5)

– 0.8 x Associated Foreign Income Taxes

0.21

These computations do not consider whether the taxpayer receives an actual benefit from the foreign taxes (or Section 250 deduction) because doing so “would involve considerable complexity.” Thus, there still may be situations where taxpayers face double taxation under the proposed rules. See Baker McKenzie, Tax New and Developments North America, Final Anti-Hybrid Rules, Jeff Rubinger and Summer Ayers LePre.

New Proposed Conduit Regulations

Conduit Regulations Generally

The conduit regulations allow the IRS to disregard a conduit entity in a conduit “financing arrangement” so that the financing arrangement is a transaction directly between the remaining parties. These rules are meant to prevent the use of a multiple party financing transaction to avoid withholding tax. Under the current conduit financing regulations, an instrument that is treated as equity for U.S. tax purposes will generally not result in a financing transaction, even if the instrument is treated as debt for foreign law purposes. The Treasury Department and the IRS determined that these types of instruments could be used inappropriately to avoid the application of the conduit financing regulations and raised similar D/NI concerns as those addressed by Sections 267A and 245A(e). The Proposed Regulations were issued to address these concerns.

Proposed Regulations

The Proposed Regulations would expand the types of equity interests treated as financing transactions to include stock or a similar interest if the tax laws of a foreign country where the issuer is resident allow the issuer to take a deduction or other tax benefit for an amount paid, accrued or distributed with respect to the stock or similar interest. Similarly, if the issuer maintains a taxable presence (“PE”) in a country that allows a deduction (including a notional deduction) for an amount paid, accrued or distributed with respect to the PE’s deemed equity or capital, then the amount of the deemed equity or capital would be treated as a financing transaction.

The Proposed Regulations would also treat equity as a financing transaction if a person related to the issuer is entitled to a refund (including a credit) or similar tax benefit for taxes paid by the issuer. If an equity interest constituted a financing translation because the issuer is allowed a NID, the Proposed Regulations would limit the portion of the financed entity’s payment that is recharatered under Treasury Regulation Section 1.881-3(d)(1)(i). The recharacterization portion would equal the financing transaction’s principal amount as determined under Treasury Regulation Section 1.881-3(d)(1)(ii), multiplied by the applicable rate used to compute the issuer’s NID in the year of the financed entity’s payment.

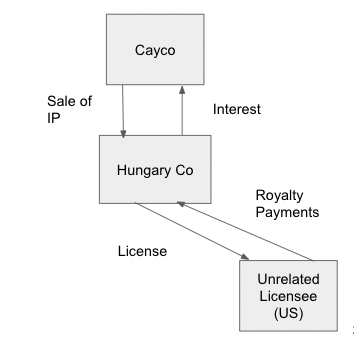

Below, please see Illustration 11 and Illustration 12 which discusses the conduit regulations.

Illustration 11.

Previously, the anti-conduit regulations generally did not attack a foreign finance company capitalized with equity under U.S. tax principles. The new proposed condit regulations could now result in FS being a condit because it is capitalized with a hybrid equity instrument. See Treas. Reg. Section 1.881-3(a)(2)(ii)(B)(1)(iv) and Baker McKenzie, Tax News and Developments, North America, Final Anti-Hybrid, Jeff Rubinger and Summer Ayers LePree.

Illustration 12.

Cayco owns valuable intellectual property and wishes to license it to an unrelated U.S. licensee. Typically, royalties from the intellectual property would be subject to 30 percent U.S. withholding tax. As a result, Cayco establishes a Hungarian corporation. The Hungarian corporation is opaque for U.S. and Hungarian purposes. Cayco sells intellectual property to the Hungarian corporation in exchange for a note. The U.S.-Hungarian tax treaty still does not have a limitation on benefits (“LOB”) provision. The treaty provides an exemption from U.S. withholding tax on royalties. The Hungarian corporation licenses the intellectual property to an unrelated U.S. licensee in exchange for royalties. The Hungarian corporation is not a hybrid entity and neither license nor note are hybrid instruments. As a result, Internal Revenue Code Section 267A does not apply to this transaction. Both license and loan are financing transactions under the conduit financing regulations. However, because the loan from Cayco to an unrelated U.S. licensee would have qualified for an exemption from U.S. withholding tax under Internal Revenue Code Section 881(c), the conduit financing rules do not apply to the above example. See Baker McKenzie, Tax News and Developments, North America, Final Anti-Hybrid Rules, Jeff Rubinger and Summer Ayers LePree.

Conclusion

The new rules governing hybrid arrangements and conduit transactions have far reaching implications on cross border transactions. While the Section 245A and 245A(e) Final Regulations provide taxpayers with some clarity, the New Proposed Regulations under the conduit rules may take some taxpayers by surprise. Particularly because the new conduit financing rules attack hybrid equity arrangements which were up until now often utilized in international transactions.

Anthony Diosdi is one of several tax attorneys and international tax attorneys at Diosdi Ching & Liu, LLP. As a domestic and international tax attorney, Anthony Diosdi provides international tax advice to individuals, closely held entities, and publicly traded corporations. Diosdi Ching & Liu, LLP has offices in San Francisco, California, Pleasanton, California and Fort Lauderdale, Florida. Anthony Diosdi advises clients in international tax matters throughout the United States. Anthony Diosdi may be reached at (415) 318-3990 or by email: adiosdi@sftaxcounsel.com.

This article is not legal or tax advice. If you are in need of legal or tax advice, you should immediately consult a licensed attorney.